In the modern world, where consumerism and instant gratification are rampant, cultivating financial discipline is more critical than ever. Financial discipline refers to the practice of managing one’s finances wisely, maintaining control over spending, saving consistently, and making informed investment decisions. It forms the backbone of financial independence and security, enabling individuals to withstand economic downturns and unexpected expenses. According to a 2023 survey by the National Endowment for Financial Education, nearly 60% of Americans say that lack of financial control is a primary source of stress. This highlights the urgent need to foster better financial habits.

Building financial discipline is not merely about restricting oneself but strategically aligning resources to meet both short-term needs and long-term goals. This article examines the key components of financial discipline, practical methods to implement them, real-world examples of success, and the evolving future of personal finance management.

Understanding the Core Principles of Financial Discipline

At its core, financial discipline involves a commitment to budgeting, saving, and responsible spending. These principles are universal but require personalized adjustments based on individual income, lifestyle, and financial goals. Budgeting serves as the foundational step, enabling individuals to track income and expenses, identify leaks in spending, and prioritize necessities over luxuries.

For instance, James, a 35-year-old software engineer, once struggled with overspending on dining out and gadget upgrades. After adopting a zero-based budgeting approach — where every dollar of income is assigned a specific purpose — he reduced his discretionary spending by 25% within six months. James redirected these savings into an emergency fund and a diversified investment portfolio, illustrating how disciplined budgeting paves the way for healthier finances.

The other pillar is saving, which requires the discipline to set aside a fixed portion of income regularly. According to the U.S. Bureau of Economic Analysis, the personal saving rate averaged 6.4% in 2022, down from 8.1% in 2021, indicating waning saving habits as the economy stabilized post-pandemic. Committing to automatic savings programs, such as employer-sponsored retirement accounts, can help maintain consistency and build wealth over time.

Techniques to Develop and Maintain Budgetary Discipline

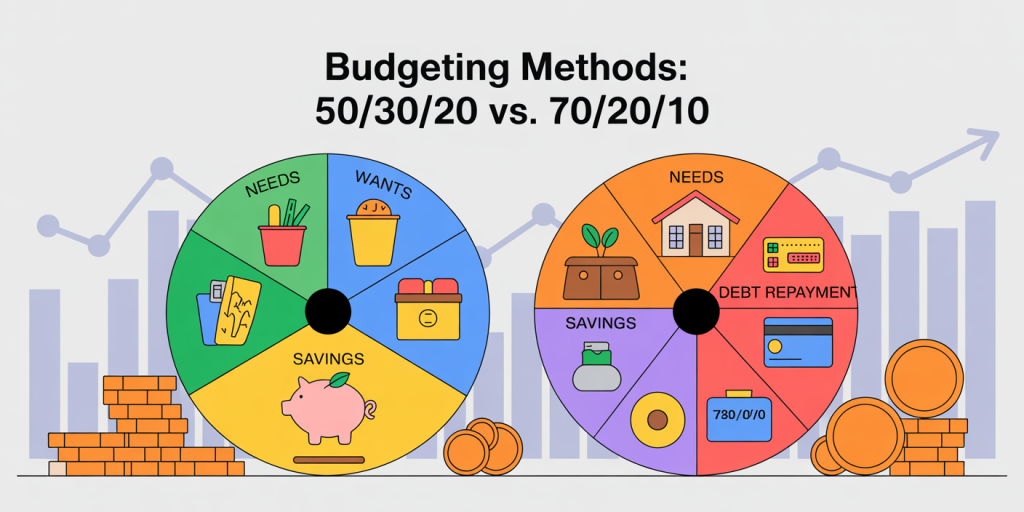

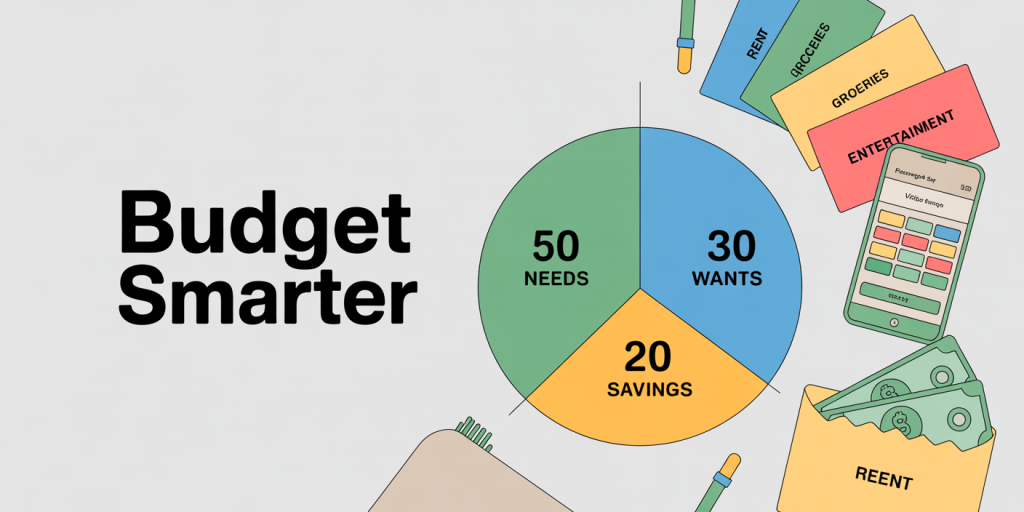

Developing a budget is often regarded as tedious, but several techniques reduce friction and increase adherence. One effective method is the 50/30/20 rule, which recommends allocating 50% of income to needs, 30% to wants, and 20% to savings or debt repayment. This rule simplifies budget creation and balances living enjoyment with financial responsibility.

Consider Emma, a young professional with a monthly income of $4,000. By applying the 50/30/20 rule, Emma assigned $2,000 to essential expenses like rent and groceries, $1,200 to discretionary spending, and $800 to her savings and loan repayment. Over time, this structure provided her clarity and momentum toward purchasing her first home.

Another practical technique is the use of budgeting apps like Mint or YNAB (You Need A Budget), which provide real-time tracking and alerts. These tools can help identify spending patterns and provide actionable insights. Research from a 2022 study in the Journal of Personal Finance shows that individuals who use budgeting applications are 30% more likely to adhere to their budgets and reduce impulse spending.

Envelop budgeting, a slightly more traditional but effective method, involves withdrawing cash assigned to specific spending categories to prevent overspending. This tangible approach can anchor spending habits, especially for those who struggle with digital tracking.

| Budget Method | Ease of Use | Effectiveness | Best For |

|---|---|---|---|

| 50/30/20 Rule | High | Moderate | Beginners looking for structure |

| Budgeting Apps | High | High | Tech-savvy users needing automation |

| Envelope Budgeting | Moderate | High | Individuals with impulse control issues |

Saving Strategies That Foster Financial Stability

Saving is more than just putting money aside — it’s about creating a financial buffer and enabling growth. One effective saving strategy is setting up separate accounts: one for emergencies, one for goals, and one for investments. This separation visually reinforces the purpose of each fund and prevents accidentally depleting critical reserves.

A 2023 report by Bankrate found that only 39% of Americans could cover a $1,000 emergency expense with savings. This statistic underscores widespread financial vulnerability. Establishing an emergency fund equivalent to three to six months of living expenses is an essential practice. For example, Sara, a single mother, automated monthly transfers of $200 to her emergency fund for two years, ultimately securing a $4,800 safety net that helped her during an unexpected medical expense, preventing debt accumulation.

Moreover, using high-yield savings accounts and certificates of deposit (CDs) can enhance returns without significant risks. Platforms like Ally or Marcus by Goldman Sachs offer interest rates 10 times above the national average savings account, enabling savers to make their money work harder.

Managing Debt with Discipline: Realistic Approaches

Debt can be a major roadblock to financial discipline; however, managing it strategically turns it from a liability to a manageable responsibility. Paying off high-interest debt first (the avalanche method) or focusing on the smallest debt first (the snowball method) are two proven strategies.

David and Laura, a married couple with combined student loan and credit card debts of $25,000, adopted the snowball method. They first targeted a $2,000 credit card balance, gaining momentum as debts disappeared one by one. This psychological boost helped them stay committed and pay off their debt in under three years.

Statistically, Americans carry $930 billion in credit card debt alone (Federal Reserve, 2024), underscoring the importance of disciplined repayment. Consolidating debt into lower-interest options, negotiating with creditors, and avoiding accumulating new debt are essential steps.

Employing budgeting methods to free cash flow for debt repayment accelerates progress. For example, reallocating the $1,200 discretionary spending described earlier by Emma toward her $15,000 student loan drastically reduced her payoff timeline.

Investing with Discipline: Building Long-Term Wealth

Investing consistently and strategically is a hallmark of financial discipline. Rather than chasing market trends or attempting to time investments, disciplined investors adopt steady approaches such as dollar-cost averaging (DCA) — investing a fixed amount periodically regardless of market conditions.

Warren Buffett famously advocates for long-term holding strategies and investing in index funds. This approach has allowed many average investors to accumulate wealth steadily. A case in point is Robert, a factory worker, who began investing $300 monthly into an S&P 500 index fund at age 30. Over 30 years, considering average returns of about 10% annually, he amassed over $900,000.

Data from Vanguard shows that DCA reduces the risk of investing at market peaks and fosters the habit of regular saving. Portfolio diversification and automated contributions through retirement accounts like 401(k) or IRAs are essential tools to ensure consistent investment discipline.

| Investment Strategy | Description | Risk Level | Ideal For |

|---|---|---|---|

| Dollar-Cost Averaging | Investing fixed sums at intervals | Low to Moderate | Beginners and steady savers |

| Lump-Sum Investing | Investing all funds at once | Moderate to High | Investors with market timing confidence |

| Index Fund Investing | Investing in broad market indices | Low | Long-term wealth builders |

| Active Stock Picking | Selecting individual stocks | High | Experienced investors willing to take risk |

Technology’s Role in Enhancing Financial Discipline

Modern technology, especially fintech solutions, plays a pivotal role in empowering financial discipline. Automated payments, personalized budgeting apps, robo-advisors, and AI-driven financial coaching offer unprecedented accessibility and convenience.

For example, robo-advisors like Betterment and Wealthfront use algorithms to create and manage diversified portfolios, lowering barriers for novice investors. Similarly, AI-powered apps such as Cleo and NerdWallet provide personalized spending insights and alerts to curb unnecessary expenses.

A 2023 Accenture report highlights that 72% of millennials prefer managing their finances via smartphone apps due to ease and real-time updates, underlining a generational shift toward digital financial discipline tools. Integrating these technological solutions into personal finance routines enhances accuracy, reduces manual errors, and offers motivation through gamification elements.

Looking Ahead: The Future of Financial Discipline

As global economies evolve, so do the challenges and opportunities related to financial discipline. Rising inflation rates, evolving job markets, and increasing reliance on technology call for adaptive financial strategies. Digitization of money, including cryptocurrencies and decentralized finance (DeFi), introduces new paradigms that disciplined individuals must navigate cautiously.

Future trends point toward greater personalization through AI, enabling tailored financial advice that adjusts dynamically to life changes. Additionally, increased financial literacy initiatives are expected to improve overall money management skills across demographics.

With increasing awareness of environmental, social, and governance (ESG) factors, responsible investing aligned with personal values will likely become a mainstream component of disciplined financial planning.

Ultimately, building financial discipline remains as relevant as ever, requiring continuous learning, adaptability, and commitment. The advent of tools and resources makes it a more achievable goal for people from all walks of life, making financial stability and independence more accessible in the decades ahead.