Money habits shape financial health and overall well-being. Unfortunately, many individuals find themselves trapped in cycles of poor money management that hinder their ability to save, invest, or simply cover monthly expenses. Breaking bad money habits may seem challenging, but with intentional strategies, achievable goals, and educated decision-making, financial transformation is possible. This article explores practical steps to identify, address, and ultimately change detrimental financial behaviors.

Understanding the Roots of Bad Money Habits

Bad money habits often stem from unconscious behaviors, emotional triggers, or lack of financial literacy. For example, impulsive buying can originate from stress relief motivations or social pressures. A 2022 study by LendingTree found that nearly 44% of U.S. consumers reported spending money to improve mood or reduce anxiety, highlighting the emotional component of money habits. Recognizing why certain habits develop is the first step toward change.

Moreover, environmental factors such as family background and cultural attitudes toward money significantly impact financial decisions. Individuals raised in households where money was a source of constant worry or conflict may adopt similar patterns. According to the National Endowment for Financial Education, financial behaviors learned in childhood contribute up to 70% of adult financial habits. This context emphasizes the need for self-reflection to unearth the origins of harmful money practices before attempting corrective action.

Identifying Your Specific Money Triggers

Pinpointing exact triggers behind bad money habits enables focused intervention. Common triggers include online shopping notifications, credit card statements arriving, or social media posts showcasing luxury lifestyles. For instance, a real case study involving a young professional, Sarah, revealed that her excessive credit card use occurred mainly after viewing influencer content on platforms like Instagram. By noting these trigger moments, Sarah began implementing mindful strategies.

One practical exercise is to keep a spending journal for two weeks, documenting every expense alongside the emotion and circumstance at the time. This method often reveals patterns, such as emotional spending during times of loneliness or using payday as an excuse for splurging on non-essentials. Armed with this knowledge, individuals can construct realistic action plans rather than vague commitments to “spend less.”

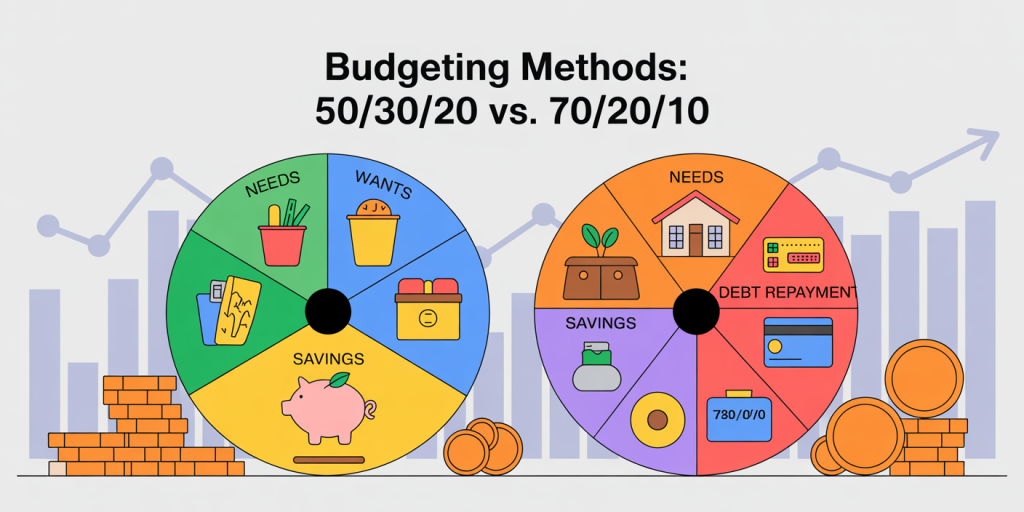

Creating Structured Budgets and Financial Plans

Once triggers are understood, establishing structured budgets plays a pivotal role in breaking bad money habits. Budgeting is not merely about restriction but about allocating resources deliberately to meet both needs and goals. According to a 2023 survey by the Pew Research Center, 68% of Americans who stuck to monthly budgets reported improvements in credit scores within one year, illustrating the tangible benefits of disciplined budgeting.

To create effective budgets, tools like the 50/30/20 rule can be adapted: 50% of income to needs, 30% to wants, and 20% to savings and debt repayment. However, individuals with poor money habits might initially need a more controlled approach, such as a 70/20/10 plan, emphasizing saving and essential expenses while minimizing discretionary spending.

| Budgeting Method | Needs (%) | Wants (%) | Savings/Debt (%) | Ideal For |

|---|---|---|---|---|

| 50/30/20 Rule | 50 | 30 | 20 | Balanced financial goals |

| 70/20/10 Rule | 70 | 20 | 10 | Those with poor money habits |

| Zero-Based Budget | 100 | 0 | 0 (All allocated) | Detailed control seekers |

For example, John, a middle-aged man burdened by credit card debt, adopted the 70/20/10 plan and systematically reduced unnecessary spending on dining out and entertainment. Within 12 months, he eliminated 60% of his credit card balance, demonstrating that precise budgeting can disrupt harmful financial routines.

Leveraging Automation to Encourage Positive Behaviors

Automation is an effective technique to counter bad money habits by reducing the reliance on willpower. Individuals can automate bill payments, savings contributions, and investment deposits. By eliminating manual interventions, they reduce the risk of late payments, impulsive withdrawals, and missed savings opportunities.

A notable example involves a couple, Emma and Mike, who struggled with inconsistent savings patterns. After setting up automatic transfers of 5% of their monthly income to a dedicated savings account, their emergency fund grew from zero to cover six months’ expenses in under two years. Data from a 2022 Bank of America report supports the efficacy: 57% of automatic savers reported feeling more in control of their finances than their non-automating counterparts.

Automating debt repayment is equally beneficial. Systems such as round-up apps, which round purchases to the nearest dollar and apply the spare change toward loans, have gained popularity. These small, consistent payments accelerate debt reduction while minimizing psychological resistance to paying large sums at once.

Reframing Mindsets and Financial Education

Shifting mindset from scarcity to abundance and from instant gratification to long-term vision is crucial. Financial education empowers individuals to make informed choices and dispel misconceptions. Unfortunately, a 2021 National Financial Capability Study revealed that only 34% of American adults demonstrated basic financial literacy, meaning most are ill-equipped to counteract ingrained bad habits.

Educational initiatives can be as simple as reading books, attending workshops, or engaging with reliable online resources. For instance, Case Study: Marcus from Seattle regularly participated in free financial literacy seminars provided by local credit unions. Over time, he developed a comprehensive understanding of credit utilization, compound interest, and investment principles, which fundamentally transformed his approach to money.

Reframing also involves cultivating patience and self-compassion. Bad money habits often come with guilt and shame, which can deter progress. Mindfulness practices combined with financial coaching can reinforce positive changes through accountability and emotional support.

Monitoring Progress and Adapting Strategies

Consistent monitoring allows for assessment of progress and recalibration of tactics. Setting measurable goals such as reducing monthly discretionary expenses by 20% or increasing savings rate by 10% can be motivating. Digital tools like budgeting apps and financial dashboards provide real-time tracking, making adjustments easier.

Consider the example of David, who began using Mint to track his spending. After three months, he noticed that his subscription services accounted for 15% of discretionary spending, a previously unnoticed expense. By canceling unused subscriptions and redirecting that money toward debt repayment, his financial situation improved considerably.

Regular check-ins with financial advisors or trusted peers can also provide valuable feedback and encouragement. Progress is rarely linear; flexibility in approach ensures that setbacks become learning opportunities rather than reasons to abandon change efforts.

Future Perspectives: Sustaining Financial Wellness Over Time

Breaking bad money habits is not a one-time event but requires ongoing commitment and adaptability as life circumstances evolve. Future financial wellness hinges on cultivating resilience against new financial stresses and temptation triggers.

Technological advancements promise to offer more personalized tools for money management, including AI-driven budgeting, predictive analytics, and behavioral finance applications that can nudge users toward better decisions. Simultaneously, cultural conversations around money are shifting, with increased openness toward discussing finances transparently, reducing stigma, and promoting financial inclusivity.

Moreover, proactive financial planning for different life stages, such as retirement or unexpected emergencies, will empower individuals to not only avoid past pitfalls but build sustainable wealth. Continuing education, paired with community support systems, can strengthen long-term financial habits.

In essence, the journey to replace bad money habits with healthy ones involves introspection, education, structured action, and perseverance. By integrating these elements with available tools and supportive environments, individuals can achieve empowered control over their finances and improve overall life satisfaction.