Money management is a vital component of a healthy relationship. When two people merge their lives, aligning their financial goals and habits can often present challenges. According to a 2019 study by SunTrust Bank, 35% of couples disagree about money, with 22% ranking finances as the leading cause of conflict. However, with open communication, transparency, and strategic planning, couples can navigate financial decisions harmoniously and build a strong economic foundation. This article explores practical ways couples can manage money effectively, drawing from expert advice, case studies, and real-world applications.

Establishing Financial Transparency

Financial transparency forms the cornerstone of successful money management in any relationship. Both partners need to openly discuss their financial status, including income, debts, expenses, and credit scores, to avoid misunderstandings later.

Take the case of Emily and James, who had been dating for three years before moving in together. Initially, their money management caused tension because James had a lower credit score due to past debts, which Emily was unaware of. After a one-on-one discussion facilitated by a financial planner, they both shared their full financial pictures and worked out a plan to handle James’s debt while saving for joint expenses.

To implement transparency, couples should schedule a “money talk” at the start of cohabitation or marriage. During this session, partners list all sources of income, monthly expenses (including personal and shared), and outstanding debts. Tools like Mint or YNAB (You Need A Budget) can help by syncing accounts, making it easier to visualize combined finances. Transparency not only minimizes surprises but also builds trust around financial decisions.

Data consistently shows that couples who practice financial transparency experience greater relationship satisfaction. A 2020 survey by SunTrust found that 60% of couples who regularly discuss money reported higher levels of intimacy and trust. This makes transparency a critical first step toward financial harmony.

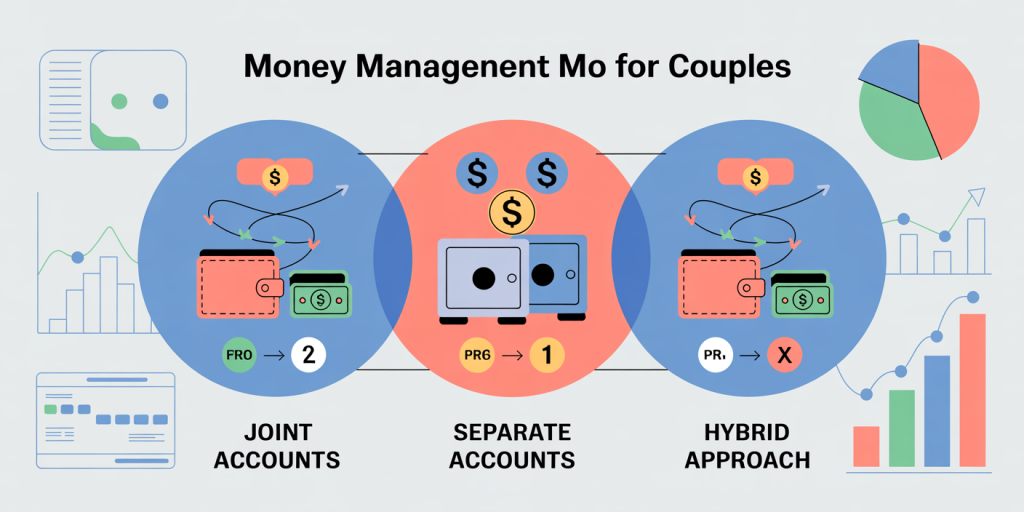

Choosing the Right Money Management System

Deciding how to combine finances is one of the most significant challenges for couples. Generally, couples can choose among three models: joint accounts, separate accounts, or a hybrid approach.

| Money Management Model | Description | Advantages | Disadvantages |

|---|---|---|---|

| Joint Accounts | Both partners pool income into shared accounts used for all expenses | Simplifies bill payments, encourages shared goals | May reduce individual autonomy, potential disagreements on spending |

| Separate Accounts | Each partner maintains their own accounts and splits shared expenses | Maintains financial independence, protects privacy | Complicates bill payments, harder to save jointly |

| Hybrid Approach | Combination of joint and separate accounts for flexibility | Balances independence and cooperation | Requires discipline and communication |

Emily and James initially used separate accounts but struggled with bill payments and felt disconnected financially. After consulting with a financial advisor, they moved to a hybrid system: they created a joint account for rent, groceries, and utilities, while keeping personal spending separate. This approach allowed them to share priorities without micromanaging each other’s money.

Choosing the right system depends on each couple’s values, communication style, and financial goals. Financial experts recommend discussing not only current preferences but also future scenarios, such as purchasing a home or having children, which might necessitate more pooled resources.

Budgeting Together for Shared Goals

A well-structured budget is essential to managing household finances and working toward shared goals. Couples who budget together are more likely to achieve financial milestones, such as buying a home or saving for retirement.

Let’s take Sarah and Miguel as an example—a couple who saved more than 20% of their joint income annually by creating a detailed budget. They started by listing all income sources and categorizing their expenses into fixed (rent, utilities) and variable (entertainment, dining out). They then set clear targets for discretionary spending and initiated monthly budget review meetings to discuss adjustments and progress.

Couples can use budgeting platforms like EveryDollar or Personal Capital to track spending and allocate funds. According to a 2021 report by the National Endowment for Financial Education, couples who budget regularly report 30% fewer money-related conflicts.

In addition, creating an emergency fund with at least three to six months of living expenses helps couples weather unexpected financial shocks without stress. For example, Sarah and Miguel agreed to build their emergency fund first before saving for other goals, ensuring financial stability during uncertainties like job changes or medical emergencies.

Handling Debt as a Team

Debt is a major source of strain for many couples. Whether it’s student loans, credit card debt, or mortgages, managing debt collaboratively is critical.

Consider the case of Priya and Daniel: Priya had significant student loans while Daniel had credit card debt. They decided to tackle their individual debts while allocating a portion of their income each month toward joint savings. This “debt snowball” method—where they paid off smaller debts first—helped maintain momentum and motivation.

According to a 2022 study by the Federal Reserve, nearly 40% of American couples carry credit card debt. Experts advise couples to openly disclose all debts during financial discussions and create a repayment plan that aligns with their overall financial strategy.

Some practical steps include consolidating high-interest debt to lower rates, negotiating with creditors, and avoiding accumulating new debt. Importantly, emotional support plays a role too: couples often succeed when debts are framed as shared challenges rather than individual burdens.

Planning for the Future: Investments and Retirement

After establishing sound budgeting and debt strategies, couples should focus on long-term financial planning. Retirement and investment decisions require alignment to ensure a secure future.

Anna and Carlos, in their early 30s, prioritized maximizing their 401(k) contributions and opening joint brokerage accounts. By consulting a financial advisor, they diversified investments based on their risk tolerance and time horizons. They also discussed the possibility of early retirement, setting benchmarks to reach their goals.

Data from the Employee Benefit Research Institute (EBRI) reveals that as of 2023, about 57% of married couples in the U.S. had saved for retirement in some form; however, many underestimate the amount required for comfortable retirement. Aligning on savings rates, investment types (stocks, bonds, real estate), and long-term goals aids couples in growing their net worth steadily.

One effective strategy involves establishing “financial checkpoints.” For example, couples might annually review investment performances, reassess retirement timelines, and adjust savings contributions. Open discussions about risk tolerance and financial ambitions help prevent conflicts related to differing attitudes toward wealth accumulation.

Future Perspectives: Evolving Financial Dynamics in Relationships

As societal norms and economic conditions evolve, so too do how couples manage their money. Trends such as increased gig economy participation, rising housing costs, and digital banking tools shape financial practices.

In the next decade, artificial intelligence-driven financial advisors and automated budgeting platforms will become more prevalent, offering tailored advice and proactive management options. Couples will likely use these technologies to optimize spending, monitor investments, and simulate financial outcomes based on various life scenarios.

Furthermore, the growing emphasis on financial equality is pushing couples to re-examine traditional money roles. Millennial and Gen Z couples, for instance, are more inclined toward egalitarian money management models, often combining finances while maintaining personal spending freedom.

Legal frameworks around cohabitation and property ownership may also influence financial arrangements. For example, jurisdictions with community property laws emphasize joint ownership of assets, requiring couples to be more deliberate about financial transparency from the outset.

Ultimately, successful money management as a couple will continue to rely heavily on communication, flexibility, and mutual respect. Couples who adapt to new tools, evolving social norms, and economic landscapes can not only reduce conflicts but also enhance their financial resilience and relationship satisfaction.

—

Effectively managing money as a couple is an ongoing process that involves openness, shared goals, and practical financial strategies. Whether establishing transparent dialogues, selecting appropriate account structures, budgeting collaboratively, tackling debt as a team, or planning for the future, couples who commit to these principles set the stage for financial and relational success. With forthcoming technological advances and evolving societal norms, couples are better equipped than ever to achieve their financial dreams together.