In the ever-evolving landscape of employment and taxation, understanding the distinctions between W-2 employees and 1099 contractors is crucial for both workers and employers. These two classifications carry significant implications for tax obligations, benefits eligibility, and legal responsibilities. Whether you are embarking on a new job, managing payroll, or planning your taxes, knowing the nuances of W-2 and 1099 forms can help you navigate financial and legal aspects with greater confidence.

The importance of correctly classifying workers extends beyond paperwork—it impacts income taxes, Social Security contributions, unemployment insurance, and even access to health benefits. For example, in 2023, the U.S. Bureau of Labor Statistics reported that approximately 10.1 million Americans worked as independent contractors, reflecting a growing trend toward flexible work arrangements. This shift means that both individuals and businesses must become well-versed in how W-2 and 1099 statuses differ and what that means in practical terms.

Understanding the Basics: What Are W-2 and 1099 Forms?

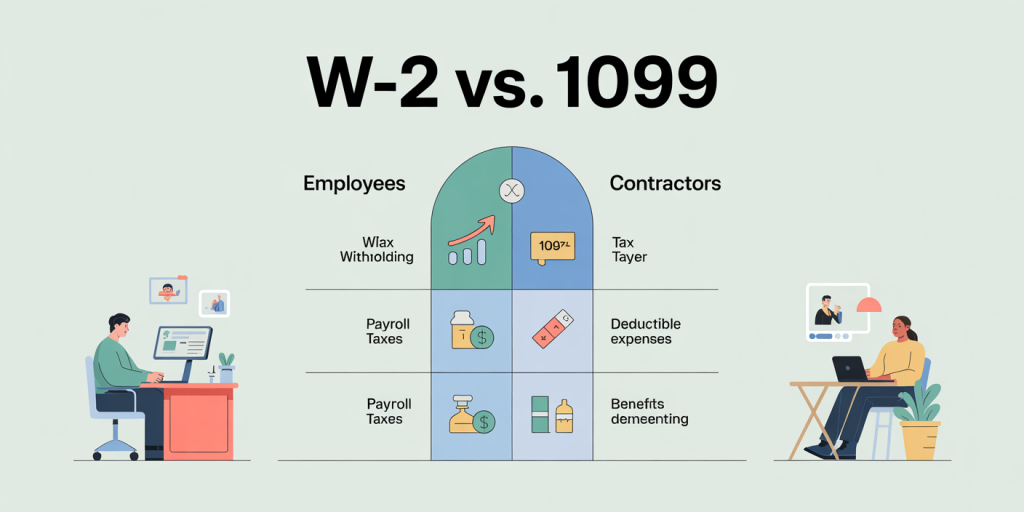

The W-2 form is used by employers to report wages paid to employees and the taxes withheld from those wages. In contrast, the 1099 form, specifically the 1099-NEC (Nonemployee Compensation), is used to report payments made to independent contractors or freelancers. The key distinction lies in the nature of the working relationship: W-2 workers are considered employees, whereas 1099 recipients are self-employed individuals or contractors.

For example, if a company hires a full-time graphic designer who works on-site, provides services per the company’s direction, and receives a regular paycheck with taxes withheld, that designer will typically receive a W-2. However, if the company hires an external freelance designer for a project-based job, paying them without tax withholding, that individual is likely to receive a 1099.

The IRS has specific guidelines on worker classification, emphasizing behavioral control, financial control, and the type of relationship. Misclassification can lead to penalties for employers and unexpected tax burdens for workers. A 2022 report from the IRS highlighted that misclassification audits recovered over $4 billion in unpaid taxes, illustrating the stakes involved.

Tax Implications for W-2 Employees and 1099 Contractors

One of the most significant differences between W-2 and 1099 statuses revolves around tax responsibilities. W-2 employees have federal, state, and payroll taxes (Social Security and Medicare) automatically withheld from their paychecks. The employer shares the burden of payroll taxes, paying matching amounts for Social Security and Medicare contributions.

Conversely, 1099 contractors are responsible for paying the full amount of self-employment taxes themselves. This amount covers both the employee and employer portions of Social Security and Medicare taxes, currently totaling 15.3%. While this seems like a heavier tax load, contractors can deduct business expenses, which can reduce their taxable income.

For instance, a 1099 contractor who earns $60,000 annually might deduct $10,000 in home office expenses, equipment, and travel related to the business, reducing the taxable income to $50,000. In contrast, a W-2 employee with the same gross income has fewer opportunities to deduct work-related expenses post the Tax Cuts and Jobs Act of 2017, which suspended many miscellaneous itemized deductions.

| Tax Aspect | W-2 Employee | 1099 Contractor |

|---|---|---|

| Tax Withholding | Employer withholds income and payroll taxes | No withholding; contractor responsible for quarterly estimated taxes |

| Payroll Taxes | Split between employer and employee | Contractor pays full self-employment tax (15.3%) |

| Deductible Expenses | Limited deduction options | Can deduct business expenses fully |

| Tax Filing Complexity | Generally simpler tax filing | More complex; may require bookkeeping |

Understanding these tax differences can help workers plan their finances more effectively, avoiding surprises during tax season.

Benefits and Protections: How Employee Status Affects You

W-2 employees often receive a broad range of benefits and protections that 1099 contractors typically do not. These benefits may include health insurance, retirement plans like 401(k)s with potential employer matching, paid time off, workers’ compensation insurance, unemployment benefits, and protections under labor laws such as minimum wage and overtime rules.

For example, Jane, a W-2 employee at a tech company, receives health insurance and 10 paid vacation days annually. When she falls ill, her employer’s sick leave policy allows her to take paid time off without income loss. In contrast, Tom, an independent contractor hired for a similar role by the same company, must obtain his own health insurance and cannot receive paid leave, illustrating a stark benefit difference.

However, 1099 contractors enjoy greater flexibility and control over their work schedules, which can result in more freedom to choose clients and projects. This autonomy is an attractive tradeoff for many freelancers and gig workers who prioritize flexibility over traditional benefits.

Legal and Compliance Considerations for Employers

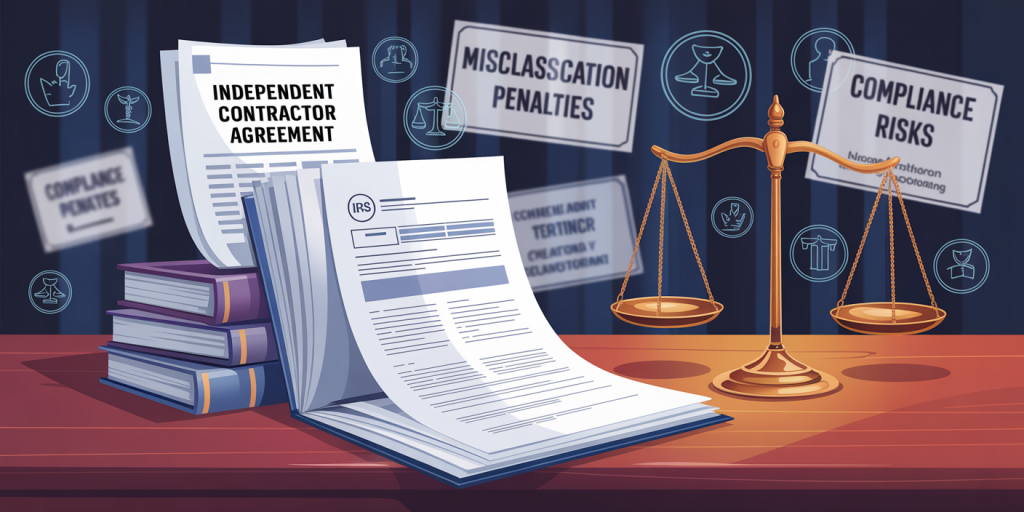

Employers must carefully assess worker classification to avoid costly legal consequences. Misclassifying W-2 employees as 1099 contractors can lead to audits, fines, back taxes, and legal liability. The IRS applies a three-pronged test assessing behavioral control, financial control, and the nature of the relationship to determine appropriate classification.

Consider a case where a delivery company hired drivers as 1099 contractors, but because the company controlled their schedules, routes, and required uniforms, a California court ruled they were employees. This misclassification led to hefty penalties and the requirement to provide retroactive benefits.

Employers are also subject to different obligations depending on classification. W-2 employees require payroll tax withholdings, workers’ compensation insurance, and unemployment tax reporting. For 1099 contractors, employers must issue 1099 forms for payments over $600 but are not required to withhold taxes or provide benefits. According to IRS data, employers who proactively audit their workforce classification reduce legal risks by up to 30%.

| Employer Obligation | W-2 Employee | 1099 Contractor |

|---|---|---|

| Tax Withholding | Mandatory | Not required |

| Benefits Provision | Often required | Not required |

| Workers’ Compensation | Required | Typically not required |

| Filing | W-2 form annually | 1099-NEC form annually |

| Risk of Misclassification | High if mislabeled as 1099 | High if true employee classified as 1099 |

Employers must maintain clear contracts and documentation to justify worker status and avoid disputes.

Financial Planning and Record-Keeping for Both Worker Types

Both W-2 employees and 1099 contractors should engage in diligent financial planning, but their approaches differ considerably. Employees typically receive consistent paychecks with taxes and benefits accounted for by their employers, simplifying budgeting and financial management. Many employers also offer payroll services that provide year-end tax documents like the W-2, consolidating reporting.

For 1099 contractors, income can be irregular and subject to volatile client payments, requiring robust record-keeping and quarterly estimated tax payments to avoid penalties. Contractors should track all business-related expenses diligently—receipts for software, travel, office supplies, and even a portion of internet service costs may qualify as deductions.

Sophia, a freelance writer, uses accounting software to track payments and expenses throughout the year, ensuring she can accurately calculate estimated taxes every quarter. This strategic planning helps prevent the common pitfall among contractors: underpayment penalties from the IRS due to improper tax advance planning.

| Financial Aspect | W-2 Employee | 1099 Contractor |

|---|---|---|

| Income Predictability | Generally stable | Often variable |

| Tax Filing Frequency | Annual | Annual plus quarterly estimated taxes |

| Expense Tracking | Minimal | Extensive; critical for tax savings |

| Financial Tools Needed | Payroll software by employer | Accounting/bookkeeping software |

Handling finances responsibly in either category reduces stress and improves compliance.

Emerging Trends and Future Perspectives in Worker Classification

The labor market continues to shift, shaped by the rise of gig economy platforms and remote work trends. Companies like Uber, DoorDash, and Upwork have popularized independent contracting as a viable employment model, raising new challenges for policymakers. In response, lawmakers and courts in various states are tightening criteria for classification, often swinging towards greater employee protections.

For example, California’s Assembly Bill 5 (AB5), enacted in 2020, established a stricter test for worker classification, impacting numerous gig workers by requiring companies to classify many as employees rather than contractors. Other states are watching closely, and federal legislation such as the proposed “Protecting the Right to Organize (PRO) Act” includes provisions that could affect classification standards nationwide.

Experts predict that as artificial intelligence and automation reshape work, new hybrid employment models may arise, blending characteristics of both W-2 employment and 1099 contracting. This evolving environment will require continuous adaptation by stakeholders.

Tax professionals, businesses, and workers should stay informed on regulatory updates and emerging court rulings to navigate this complex space successfully. Digital platforms offering streamlined tax services and compliance tools are expected to grow in prominence, easing burdens on independent contractors and small businesses alike.

—

In summary, understanding the differences between W-2 employees and 1099 contractors is essential for effective tax planning, legal compliance, and career development. Each classification carries unique responsibilities and opportunities, deeply influencing financial stability and access to benefits. As the workforce landscape evolves, staying informed and adaptable will remain key to thriving in this dynamic environment.