The growing trend of the FIRE movement—an acronym for Financial Independence, Retire Early—has captivated the attention of millions worldwide, particularly millennials and Gen Z. Rooted in the desire to break free from traditional employment and achieve financial freedom well before the standard retirement age, this movement reshapes how people perceive work, money, and life balance. Understanding FIRE thoroughly sheds light on a lifestyle many aspire to but few fully understand.

The FIRE philosophy emphasizes aggressive saving, disciplined investing, and frugal living to amass sufficient wealth that facilitates early retirement. For many, the ultimate goal extends beyond simply quitting the 9-to-5 grind; it is about attaining autonomy, reducing stress, and gaining time for passion projects or personal growth.

Origins and Core Principles of the FIRE Movement

The FIRE movement gained traction after the publication of financial blogger Mr. Money Mustache in 2011, whose writing inspired readers to rethink their approach to money and lifestyle. This movement builds upon principles of personal finance that stress high savings rates and intelligent investing.

At its core, FIRE proponents aim to save between 50% and 75% of their income instead of the traditional 10-15%. The saved money is then invested, usually in low-cost index funds, to generate passive income that covers living expenses over time. The “4% rule” often guides these calculations: once your investment portfolio can safely withdraw 4% annually to cover costs, you achieve financial independence.

An illustrative case is that of Joe and Jenny, a couple from Texas who managed to retire at age 40 by adopting a high-saving lifestyle early in their careers. They prioritized paying off debt and limited lifestyle inflation despite income raises. By their mid-30s, their investment portfolio had grown to over $1 million, allowing them to retire early and pursue creative endeavors without financial worry.

Variants Within the FIRE Movement

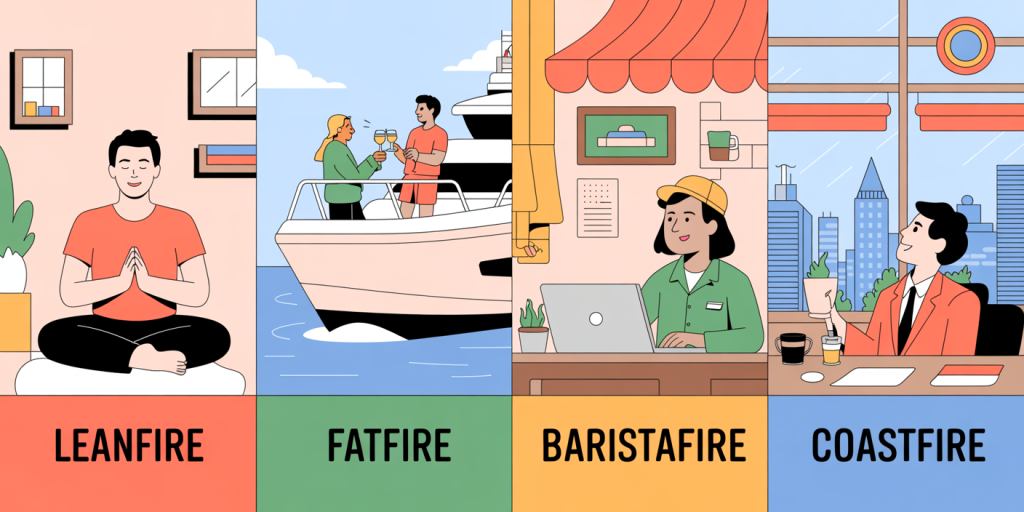

While the phrase FIRE suggests a singular approach, the movement comprises various subcategories tailored to different savings goals, risk levels, and lifestyle desires. Understanding these provides a clearer path for individuals interested in the movement. LeanFIRE: Focuses on extreme frugality to retire early with a smaller nest egg, sometimes under $500,000. Practitioners accept a minimalist lifestyle and lower annual expenses, often under $25,000. FatFIRE: This path involves accumulating more substantial wealth—often exceeding $2 million—which enables a comfortable or even luxurious retirement lifestyle. FatFIRE participants target more flexibility and higher yearly spending. BaristaFIRE: A hybrid approach where retirees partially withdraw from savings early while continuing part-time work to cover some expenses. This reduces the initial portfolio size required and lowers risk. CoastFIRE: Achieved when investments have grown enough that future contributions are no longer necessary. Individuals working full-time but financially independent in the sense that their savings will grow sufficiently for retirement.

The following comparative table summarizes these variations:

| Variant | Nest Egg Size | Annual Spending Estimate | Lifestyle Example | Work Status |

|---|---|---|---|---|

| LeanFIRE | <$500,000 | <$25,000 | Minimalist housing, low discretionary spend | Fully retired, frugal |

| FatFIRE | >$2,000,000 | >$75,000 | Comfortable housing, travel, dining out | Fully retired, affluent |

| BaristaFIRE | Varies (smaller) | Partial self-support | Part-time work, moderate expenses | Semi-retired, part-time |

| CoastFIRE | Mid-range | Future portfolio growth covers expenses | Full-time job ongoing, no new savings needed | Working full-time |

The choice among these depends largely on personal values, risk tolerance, and desired quality of life.

Financial Strategies Underpinning the FIRE Movement

Achieving FIRE is rarely accidental; it demands rigorous financial planning and smart strategies. Several key practices stand out.

Aggressive Savings and Budget Control

Achieving the high savings rates necessary often means cutting back on discretionary expenses. This can include downsizing housing, limiting dining out, or avoiding expensive habits like brand-new cars. For example, Mr. Money Mustache famously avoided car ownership altogether, biking instead for transportation, which notably reduced his living costs.

Data from the U.S. Bureau of Economic Analysis shows that the average U.S. savings rate in 2023 hovered around 7.5%, while FIRE adherents commonly save 50% or more. The discipline required for this difference is critical and often the most challenging part of the journey.

Investing for Growth and Passive Income

Sustained investment returns are essential for FIRE success. Most adherents favor low-cost index funds, which track the market and reduce fees. Historically, the S&P 500 has returned an average of approximately 7-10% annually after inflation.

Real-world evidence is seen in cases like Vicki, an engineer who retired at 38 by maxing out her 401(k) and investing in diversified index funds. Despite market fluctuations, she focused on long-term growth rather than timing, which built her portfolio steadily.

Debt Reduction and Avoidance

Debt, especially high-interest credit card debt, can derail FIRE plans. Prioritizing paying down debt early prevents interest accumulation, freeing up income for investment. For example, Sam accelerated mortgage payments to save thousands in interest, enabling earlier independence.

Side Hustles and Passive Revenue Streams

Many FIRE practitioners supplement their income through gigs, freelancing, or rental properties before fully retiring. Flexible income can accelerate savings or continue supporting lifestyle expenses after retirement. Natalie, a freelance graphic designer, used side work to build a six-figure portfolio that allowed her to reduce full-time hours by 50% and transition gradually into retirement.

Psychological and Social Considerations

While financial tactics are paramount, the FIRE movement also involves significant emotional and social adjustments.

Lifestyle Sacrifice and Mindset Shift

Cutting expenses dramatically or avoiding social norms around consumption can lead to feelings of missing out. Several studies highlight that maintaining “frugal but fulfilling” lifestyles is key to avoiding burnout or regret. Community forums like Reddit’s r/financialindependence often discuss emotional strategies to stay motivated.

Moreover, early retirees may struggle with identity loss or lack of structured purpose. Some solve this by dedicating time to hobbies, volunteering, or entrepreneurial ventures.

Societal Impact and Norm Challenges

Choosing FIRE can strain personal relationships, especially in cultures where work identity is strongly tied to social status. For example, some family members may criticize early retirement as irresponsible. Balancing these pressures requires resilience and clear communication.

Furthermore, FIRE can subtly challenge economic structures reliant on continuous workforce participation, but its overall societal impact remains limited given its niche demographic.

Risks and Criticisms of the FIRE Approach

Despite its appeal, FIRE is not without challenges and critics have raised valid concerns.

Market Dependency and Sequence of Returns Risk

Relying on investment returns exposes adherents to market downturns. Early retirees withdrawing during a recession risk depleting portfolios prematurely—a phenomenon known as “sequence of returns risk.” For instance, someone retiring in 2008 without a contingency plan could have struggled significantly.

Some FIRE enthusiasts use conservative withdrawal rates or hold cash reserves to mitigate this. Others adopt part-time work post-retirement to buffer volatility.

Healthcare and Inflation Concerns

Inconsistent healthcare coverage and inflation over decades can erode living standards. According to the Employee Benefit Research Institute, healthcare expenses often increase with age, and early retirees must plan for these rising costs carefully.

Lifestyle Sustainability

Extreme frugality is difficult to maintain, and some early retirees report scaling up spending after retirement, complicating financial forecasts. A 2022 survey showed 30% of early retirees increased annual expenses by more than 20% within five years of retirement.

Future Perspectives of the FIRE Movement

The FIRE movement continues to evolve as economies and social norms shift. Technological advances like robo-advisors and financial apps make disciplined investing and tracking easier, potentially broadening participation.

Moreover, environmental and social consciousness influence new FIRE adherents toward integrating sustainability with financial planning. Concepts like “Slow FIRE” emphasize balancing frugality with quality of life, avoiding burnout.

As remote work becomes increasingly mainstream, people can relocate to lower-cost regions to accelerate FIRE goals. This geoarbitrage trend may reshape labor markets and lifestyle choices globally.

Financial education improvements at earlier stages will likely support more realistic FIRE planning among younger generations. Policymakers may eventually respond by adjusting retirement frameworks or tax incentives to address this demographic shift.

Despite challenges, FIRE appeals to universal desires for control, freedom, and purpose. Its future will likely include more personalized and flexible approaches that accommodate diverse life trajectories.

—

In summary, the FIRE movement represents a powerful, multifaceted approach to personal finance that combines saving, investing, and lifestyle choices to achieve early financial independence. It demands commitment, resilience, and thoughtful planning but offers transformative possibilities for those willing to embrace its philosophy. By understanding its variants, principles, and risks, individuals can better assess whether FIRE aligns with their values and aspirations—and chart a path toward financial empowerment.