Understanding the banking system is crucial for anyone interested in economics, finance, or simply managing personal finances effectively. Banks play a vital role in the economy by facilitating financial transactions, providing loans, and acting as custodians of money. This article explores how the banking system operates, its core functions, the key players involved, and current trends shaping the future of banking worldwide.

The Fundamentals of Banking: Roles and Operations

Banks serve as intermediaries between savers and borrowers, providing a secure place to deposit money and access to credit when needed. At its core, the banking system enables efficient capital allocation, channeling funds from those with surplus capital to those requiring funds for consumption or investment. This process fosters economic growth by supporting businesses, infrastructure projects, and consumer spending.

One primary function of banks is accepting deposits from customers, which form the base of their lending activities. These deposits are often divided into categories such as checking accounts, savings accounts, and certificates of deposit (CDs). According to the World Bank data from 2022, global deposits in commercial banks reached over $60 trillion, highlighting the immense scale at which banks operate. Banks then use these deposits to extend loans to individuals and businesses, charging interest rates higher than what they pay depositors—a mechanism generating profit for banks while incentivizing deposit growth.

How Banks Create Money Through Lending

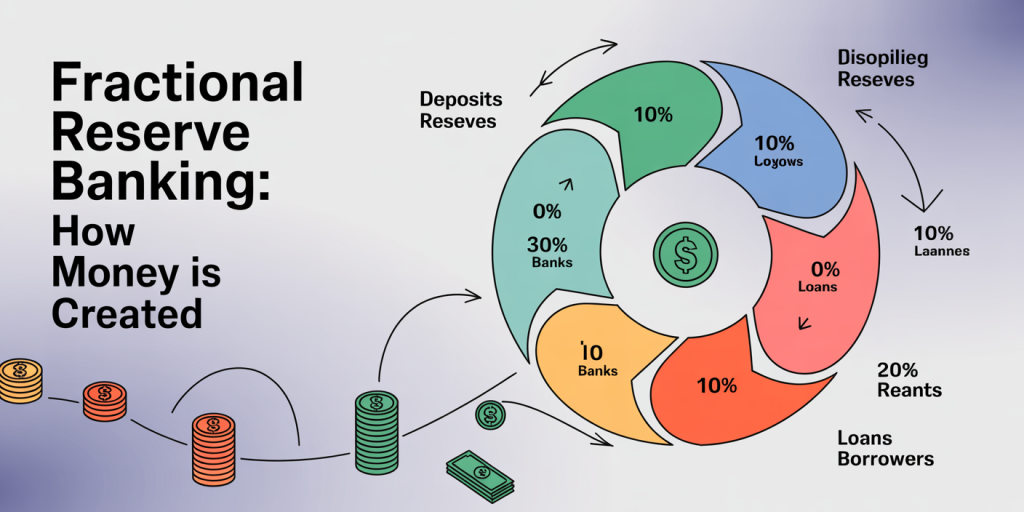

An essential but often misunderstood aspect of banking is the mechanism of money creation. When a bank issues a loan, it does not simply transfer existing money but actually creates new deposit money. This process is known as fractional reserve banking, wherein banks only keep a fraction of deposits as reserves and lend out the remainder.

For example, if a bank receives a $1,000 deposit and the reserve requirement is 10%, it must keep $100 but can lend out $900. The borrower then typically spends this loan, and the recipient deposits the funds back into the banking system, creating further deposits and loans. Through this multiplier effect, the initial deposit results in a total increase in money supply that can be up to ten times the original amount, depending on the reserve ratio and other regulatory measures.

The impact of money creation is substantial in the economy, influencing inflation and interest rates. The Federal Reserve (Fed) in the United States controls reserve requirements and uses monetary policy tools to regulate this process to ensure economic stability.

Types of Banks and Their Functions

The banking system comprises various types of institutions, each serving specific roles within the economy. Commercial banks are the most common; they focus on retail banking services such as accepting deposits, providing business and consumer loans, mortgages, and credit cards.

Investment banks, on the other hand, specialize in underwriting securities, facilitating mergers and acquisitions, and offering advisory services to corporations and governments. These banks do not typically take deposits from the public but help companies raise capital in financial markets.

Central banks such as the European Central Bank (ECB) or the Bank of England play a regulatory and supervisory role. They manage the country’s monetary policy, supervise commercial banks to ensure solvency, and act as lenders of last resort during financial crises. Central banks are responsible for maintaining financial stability and controlling inflation by adjusting interest rates and implementing quantitative easing or tightening policies.

Below is a comparative table summarizing the main differences between these bank types:

| Type of Bank | Primary Functions | Customers | Revenue Sources | Key Examples |

|---|---|---|---|---|

| Commercial Banks | Deposit taking, lending | Individuals, businesses | Interest from loans, fees | JPMorgan Chase, Deutsche Bank |

| Investment Banks | Securities underwriting, advisory | Corporates, governments | Fees, trading commissions | Goldman Sachs, Morgan Stanley |

| Central Banks | Monetary policy, bank supervision | Government, banks | Interest on reserves, policy tools | Federal Reserve, ECB |

The Banking System in Action: Real-World Examples

To illustrate how banking functions on the ground, consider the case of the 2008 Global Financial Crisis. Excessive lending by commercial banks to risky borrowers, especially in the U.S. mortgage market, demonstrated the risks embedded in banking operations. Banks like Lehman Brothers had large exposure to high-risk mortgage-backed securities, and when borrowers defaulted in massive numbers, the resulting losses triggered a liquidity crisis. This required central banks worldwide to intervene with emergency measures, including lowering interest rates and providing bailout packages.

On a more positive note, consider microfinance banks in developing countries such as the Grameen Bank in Bangladesh. These institutions focus on providing small loans to low-income individuals who lack access to traditional banking. This form of banking has helped millions escape poverty by enabling entrepreneurship and financial inclusion.

The Role of Technology in Modern Banking

Technology has transformed how banks operate, making transactions faster, more secure, and accessible globally. Online and mobile banking platforms have replaced many traditional branch services, allowing customers to check balances, transfer funds, and apply for loans from their smartphones.

The rise of fintech companies exemplifies this innovation. Fintech firms utilize blockchain, artificial intelligence (AI), and data analytics to streamline services and reduce operational costs. For example, digital wallets like PayPal and mobile payment platforms such as Apple Pay have made cashless transactions ubiquitous.

Furthermore, the adoption of blockchain technology is reshaping banking by enabling transparent and tamper-proof record-keeping. Banks are experimenting with cryptocurrencies and decentralized finance (DeFi) models, potentially reducing reliance on centralized intermediaries.

Despite these advances, cybersecurity remains a critical concern. Banks invest heavily in protecting customer data against breaches and fraud, given how sensitive financial information is. The 2023 IBM report indicated that the financial sector accounted for nearly 20% of all cyberattacks globally, emphasizing the need for robust security protocols.

Regulatory Environment and Its Impact on Banking Stability

Banks operate under stringent regulations designed to safeguard the financial system and protect depositors’ funds. Key regulatory frameworks include Basel III standards, enforced globally, which require banks to maintain sufficient capital reserves and manage risks prudently.

Compliance with these regulations affects how banks manage their balance sheets and interact with customers. For example, after the 2008 crisis, many countries tightened lending criteria to reduce the risk of default. Stress testing, an evaluation of a bank’s resilience to economic shocks, became a standard practice for regulators worldwide.

In the United States, the Dodd-Frank Act introduced significant reforms to increase transparency and accountability in the financial sector. Its provisions include enhanced oversight of derivatives trading and stricter separation between investment and commercial banking activities via the Volcker Rule.

Table: Key Banking Regulations Globally

| Regulation | Region | Purpose | Impact on Banks |

|---|---|---|---|

| Basel III | Global | Capital adequacy, risk management | Higher capital reserves, liquidity buffers |

| Dodd-Frank Act | United States | Financial stability, consumer protection | Increased compliance costs, risk reduction |

| PSD2 | European Union | Payment services, open banking | Promotes competition, data sharing with third parties |

| FATCA | Global (US focus) | Tax compliance by foreign financial institutions | Reporting requirements, transparency |

Future Perspectives: Innovation and Challenges Ahead

The banking system is on the cusp of transformative change, driven by evolving consumer expectations, regulatory shifts, and technological innovation. Open banking initiatives, which encourage banks to share data securely with authorized third parties, aim to foster competition and create personalized financial services.

Artificial intelligence will play an increasingly significant role in credit scoring, fraud detection, and customer service. Robo-advisors that use algorithms to manage investment portfolios are already gaining popularity, reducing costs and democratizing wealth management.

Simultaneously, the rise of cryptocurrencies and decentralized finance presents both opportunities and challenges. While digital currencies can increase transaction speed and lower costs, regulatory uncertainties and volatility remain barriers. Central bank digital currencies (CBDCs) are being explored and piloted in countries like China, which could redefine how banks interact with the monetary system.

Sustainability is another emerging priority. Banks are integrating environmental, social, and governance (ESG) criteria in lending and investment decisions, reflecting growing concern about climate change and ethical finance.

In conclusion, the banking system is a complex network of institutions, regulations, and technologies working together to facilitate economic activity. Its evolution will likely continue to be shaped by innovation, regulatory responses, and global economic dynamics, making understanding it ever more important for individuals and businesses alike.