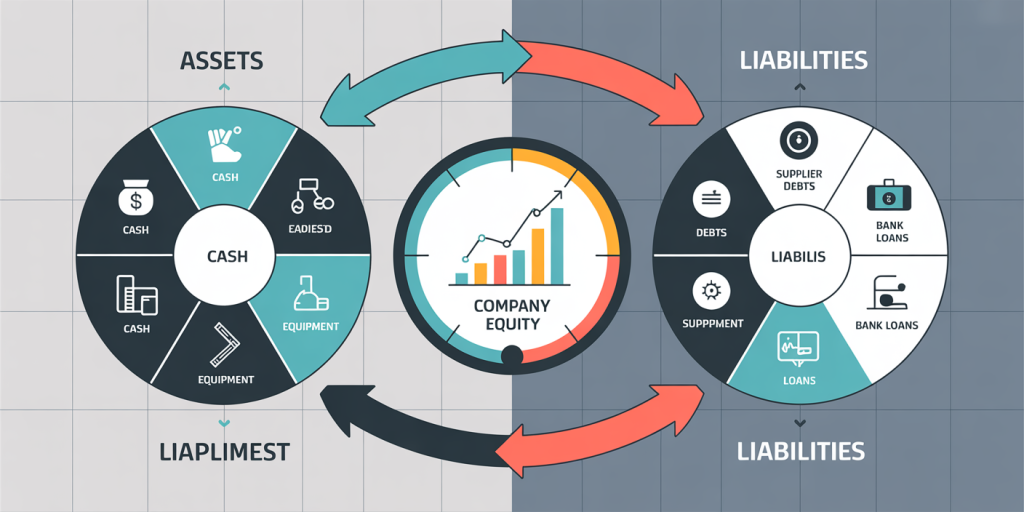

In the world of finance and accounting, understanding the distinction between assets and liabilities is fundamental. These two concepts form the backbone of financial statements and play a critical role in evaluating an organization’s financial health. Whether you are a business owner, investor, or student of finance, mastering the difference between assets and liabilities can help you make informed decisions, improve cash flow management, and assess profitability accurately.

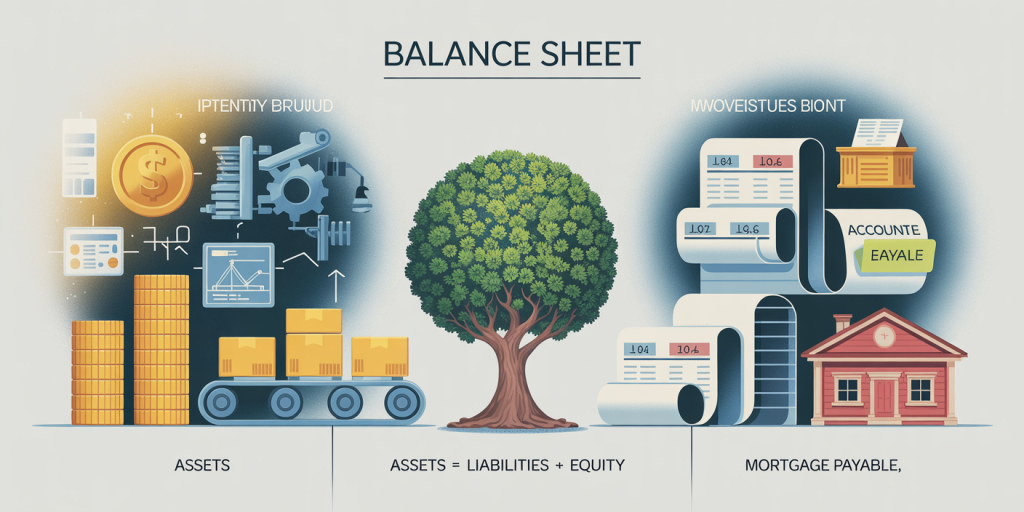

Assets and liabilities are often presented side by side on the balance sheet, where they illustrate what a company owns versus what it owes. The balancing act between these two elements ultimately determines the net worth or equity of a business. To fully grasp their significance, it’s essential not only to define each term but also to explore their types, examples, and implications in practical scenarios.

Defining Assets and Liabilities: Core Concepts

Assets are resources that a company or individual owns and expects to generate future economic benefits. They are valuable items or rights that can increase wealth either through direct use or by conversion to cash. Assets include both tangible items like machinery and intangible ones such as patents or trademarks.

For example, a business might own office equipment valued at $50,000, inventory worth $100,000, and have a $20,000 account receivable from customers. Each of these represents an asset because they are economic resources that can help the company earn revenue or be liquidated for cash if needed.

On the other hand, liabilities represent obligations or debts owed to outsiders or creditors. These are claims that others have against the company’s assets and must be settled through the transfer of economic resources such as cash, goods, or services. Essentially, liabilities quantify what the company owes.

For instance, if a business owes $30,000 on a bank loan and has outstanding supplier invoices totaling $15,000, these amounts constitute liabilities. They denote future economic sacrifices that the company must fulfill.

Together, assets and liabilities provide a snapshot of ultimate financial equilibrium through the accounting equation: Assets = Liabilities + Equity

This equation highlights that assets are financed either by borrowing (liabilities) or through owner’s investment (equity).

Types of Assets: Understanding Their Categories and Functions

Assets can be broadly classified into current assets and non-current (or fixed) assets, based on their liquidity and usage duration.

Current assets are expected to be converted into cash, sold, or consumed within a year. These typically include cash and cash equivalents, accounts receivable, inventory, and short-term investments. Their high liquidity allows businesses to meet day-to-day operational expenses promptly.

Consider a retail store where inventory turnover is crucial. The merchandise it holds is a current asset since it will be sold and converted into cash within a relatively short period.

Non-current assets, in contrast, are long-term investments used to produce goods or services. These include property, plant and equipment (PP&E), intangible assets such as copyrights and patents, and long-term investments. These resources are not readily convertible to cash and provide value over several years.

An example is a manufacturing company that invests $500,000 in machinery with an expected useful life of 10 years. This asset aids production but cannot easily be transformed into cash in the short term.

According to data from the U.S. Small Business Administration (SBA), effective asset management helps boost business growth by improving liquidity ratios and operational efficiency. Maintaining a balanced portfolio of current and fixed assets ensures companies have sufficient funds to cover debts and invest in future opportunities.

Types of Liabilities: Short-Term vs. Long-Term Obligations

Liabilities are divided into current liabilities and long-term liabilities, depending on their due dates.

Current liabilities are obligations due within one year. Common examples include accounts payable, wages payable, short-term loans, and accrued expenses. These items require timely settlement to maintain the company’s creditworthiness and operational stability.

For example, a company may owe suppliers $40,000, which must be paid within 30 days. This amount is a current liability, and failure to pay can strain supplier relationships and impact inventory procurement.

Long-term liabilities represent debts payable beyond one year, such as mortgages, bonds payable, and long-term bank loans. These obligations finance significant capital expenditures or expansions and must be managed over the long haul.

A real estate company might take out a 20-year mortgage to finance property acquisition. This mortgage constitutes a long-term liability and influences long-term financial planning and risk assessment.

According to the Financial Accounting Standards Board (FASB), recognizing the distinction between short- and long-term liabilities is critical for assessing solvency and liquidity, key indicators used by creditors and investors.

Practical Examples Illustrating Assets and Liabilities

To solidify the understanding of assets versus liabilities, examining practical cases from different sectors offers valuable insights.

Example 1: Tech Startup

A technology startup may have the following: Assets: $200,000 in software licenses (intangible asset), $50,000 in office equipment, and $75,000 in cash. Liabilities: $100,000 loan from investors, $20,000 owed to vendors.

The company’s equity arising from this scenario equals assets minus liabilities: ($200,000 + $50,000 + $75,000) – ($100,000 + $20,000) = $205,000. This figure indicates the net value held by owners after satisfying all debts.

Example 2: Manufacturing Firm

A manufacturing firm holds: Assets: $1 million in factory machines, $500,000 in raw materials, and $300,000 in accounts receivable. Liabilities: $600,000 mortgage on factory buildings, $200,000 in short-term supplier debt.

Their total equity is ($1,000,000 + $500,000 + $300,000) – ($600,000 + $200,000) = $1,000,000.

These examples illustrate how assets reflect resources under control, while liabilities show obligations to external parties. The difference between the two is the company’s equity, signaling its financial stability and potential for growth.

Comparative Overview: Assets vs. Liabilities

A comparative table can help differentiate assets and liabilities clearly:

| Aspect | Assets | Liabilities |

|---|---|---|

| Definition | Economic resources owned | Economic obligations owed |

| Purpose | Generate future economic benefits | Settle debts and finance operations |

| Classification | Current and non-current (fixed) | Current and long-term |

| Impact on Cash Flow | Positive inflows (e.g., sales, liquidations) | Outflows for repayments and expenses |

| Examples | Cash, inventory, equipment, patents | Loans, accounts payable, mortgages |

| Appearance on Balance Sheet | Left side (debit) | Right side (credit) |

| Effect on Equity | Increase equity when acquired | Decrease equity as debts are paid off |

This table highlights essential features that distinguish assets from liabilities and their respective roles in a company’s financial architecture.

Importance of Managing Assets and Liabilities

Proper asset and liability management (ALM) is vital for safeguarding a company’s financial health. Firms must balance these elements to ensure they have enough assets to cover their liabilities while optimizing returns on investments.

For instance, excessive liabilities without corresponding assets can cause insolvency risks. The 2008 financial crisis demonstrated how over-leveraging (high liabilities) without adequate asset backing led to bankruptcies and widespread economic disruption.

Conversely, holding too many idle assets, such as excess inventory or unused equipment, can burden working capital and reduce profitability. Research from Deloitte highlights that companies with intelligent ALM processes experience 20-30% better liquidity ratios and improved market valuation.

Financial institutions often use ALM to match the maturity profiles of their assets and liabilities. For example, banks ensure that the interest rates and timelines of their loans (assets) correspond with those of their deposits and borrowings (liabilities), reducing the risk of liquidity shortfall.

Future Perspectives on Assets and Liabilities

As technology and market dynamics evolve, the classification and management of assets and liabilities are likely to undergo significant changes.

Digital transformation has introduced new asset types, such as cryptocurrencies and digital intellectual property, challenging traditional accounting practices. According to PwC’s 2023 Global CEO Survey, 65% of executives are investing heavily in intangible assets, which now represent over 50% of the market value of companies in the S&P 500, compared to just 17% in the 1970s.

On the liabilities front, emerging issues like climate-related risks and regulatory changes could alter how companies assess contingent liabilities and disclosures. The increased focus on sustainability demands transparency in environmental liabilities, which were previously unquantified.

Artificial intelligence and blockchain technologies promise enhanced asset verification and real-time liability tracking, potentially revolutionizing financial reporting and risk management. These innovations can enable instantaneous asset valuation and improve the accuracy of liability recognition, fostering trust and efficiency in financial markets.

In summary, while the fundamental difference between assets and liabilities remains the same—they represent resources owned versus obligations owed—the scope and management techniques will continue to adapt to the evolving economic and technological environments. Mastery of these concepts will remain indispensable for financial professionals navigating the complexities of tomorrow’s business landscape.