Net worth is an essential financial metric that serves as a vital indicator of an individual’s or organization’s fiscal condition. Whether you are planning for retirement, managing personal finances, or running a business, understanding your net worth can help you make informed decisions, gauge progress toward financial goals, and prepare for uncertainties. This article delves into the concept of net worth, its components, practical examples, and how it compares across various situations, providing you with a clear framework for assessing and improving your financial standing.

The Basics of Net Worth: What Does It Really Mean?

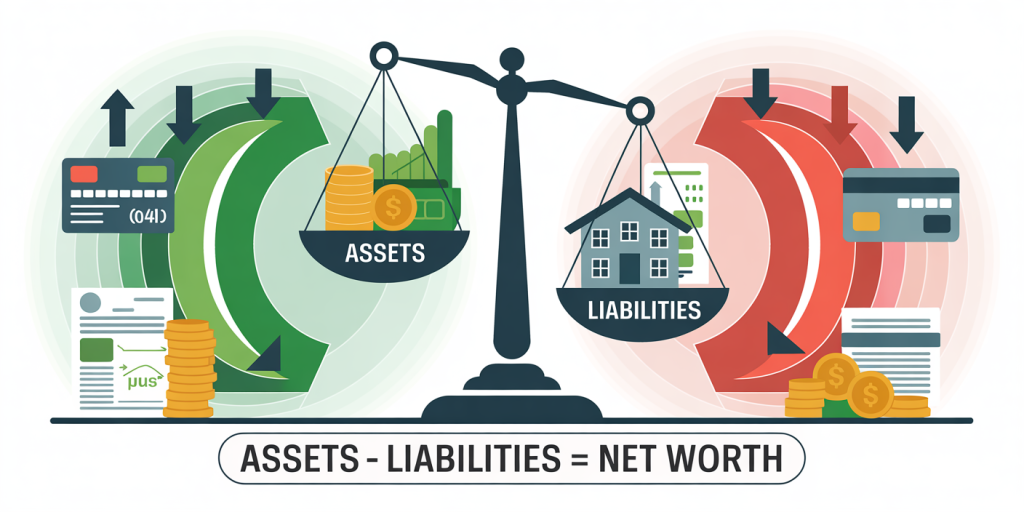

At its core, net worth is the total value of everything you own minus all your debts. In simple terms, it is calculated as:

Net Worth = Total Assets – Total Liabilities

Assets include cash, investments, real estate, vehicles, retirement accounts, and personal property of value. Liabilities, on the other hand, cover mortgages, credit card balances, student loans, car loans, and other outstanding debts. This straightforward formula provides an immediate snapshot of financial health, revealing whether you are in a positive or negative position.

To illustrate, consider two individuals: Amy and Brian. Amy owns a home worth $300,000, has $50,000 in investments, and $20,000 in cash savings. She owes $200,000 on her mortgage and $10,000 in credit card debt. Amy’s net worth would be:

Assets = 300,000 + 50,000 + 20,000 = $370,000 Liabilities = 200,000 + 10,000 = $210,000 Net Worth = 370,000 – 210,000 = $160,000

Brian, meanwhile, rents his home and has $100,000 in student loans with no significant assets. His net worth is negative:

Assets = $0 Liabilities = $100,000 Net Worth = 0 – 100,000 = -$100,000

In this example, Amy’s positive net worth suggests she is building financial stability, while Brian’s negative net worth indicates a debt burden that needs managing.

Why Tracking Net Worth Matters

Understanding your net worth provides much more than just a number—it offers insight into your financial trajectory. Regularly monitoring net worth helps identify trends: Are you accumulating assets faster than liabilities? Are debts rising in a way that could jeopardize future financial security?

According to a 2023 Federal Reserve report, the average American household had a median net worth of approximately $121,700. However, this median hides significant disparities: the top 10% of households had a median net worth approaching $1.9 million, while the bottom 25% faced near-negative net worth. By evaluating your own net worth against national averages or peer groups, you can set realistic goals and benchmarks for financial growth.

Moreover, net worth is crucial for planning retirement. For instance, a 2022 Vanguard study showed that individuals aiming for a comfortable retirement often need a net worth 10-12 times their annual income saved by retirement age. Without net worth awareness, it is difficult to determine if retirement savings are on track.

Components of Net Worth: Deep Dive into Assets and Liabilities

Understanding Assets

Assets are everything you own that has monetary value. They are generally categorized as either liquid or illiquid: Liquid assets: Cash or assets easily convertible to cash, such as savings accounts and stocks. Liquid assets provide immediate financial flexibility in emergencies. Illiquid assets: Items that cannot easily be turned into cash without affecting their value, such as real estate, cars, and retirement accounts.

It is vital to consider the market value of assets, not just their purchase price. For example, if you bought a car for $30,000 five years ago, but it now has an estimated worth of $12,000, your asset valuation should reflect the current market price.

Liabilities: Understanding Debt Types

Liabilities include all debts owed, which may be short-term or long-term: Short-term liabilities: Credit card balances, utility bills, or personal loans due within one year. Long-term liabilities: Mortgages, student loans, auto loans, and other debts with extended terms.

Not all debt is necessarily harmful. For instance, a mortgage often reflects an investment in property that may appreciate. High-interest debt, like credit cards, can damage net worth if left unmanaged.

The following table offers an overview of common asset and liability types, with examples:

| Category | Examples | Nature |

|---|---|---|

| Assets (Liquid) | Cash, savings accounts, stocks | Easily accessible |

| Assets (Illiquid) | Real estate, retirement funds | Difficult to convert quickly |

| Liabilities (Short-term) | Credit card debt, bills | Due within a year |

| Liabilities (Long-term) | Mortgages, student loans, car loans | Payment over several years |

By regularly assessing these components, individuals can understand which parts of their financial profile dominate their net worth and take appropriate action.

How Net Worth Varies Across Life Stages and Net Worth Benchmarks

Net worth trajectories differ significantly with age, income, and life circumstances. Young adults facing student debt and limited assets may have a negative net worth, whereas mid-career professionals typically accumulate net worth through homeownership, investments, and retirement savings.

According to the Federal Reserve’s “Survey of Consumer Finances” data from 2022, median net worth tends to grow with age, peaking in the 55-64 age group at around $200,000 median net worth before leveling off or declining in retirement years:

| Age Group | Median Net Worth (USD) |

|---|---|

| Under 35 | $13,900 |

| 35-44 | $91,900 |

| 45-54 | $168,600 |

| 55-64 | $212,500 |

| 65-74 | $266,400 |

| 75+ | $254,800 |

Note that while median values give insight into typical households, top earners may have exponentially higher net worth.

A practical example involves Sarah, 30, who recently graduated and has $40,000 in student loans and minimal savings. Her net worth is negative, but with steady income, saving discipline, and investing, Sarah can increase net worth through the decades. By contrast, John, 60, owns a home fully paid off and has accumulated $750,000 in retirement accounts, presenting a strong net worth for his age.

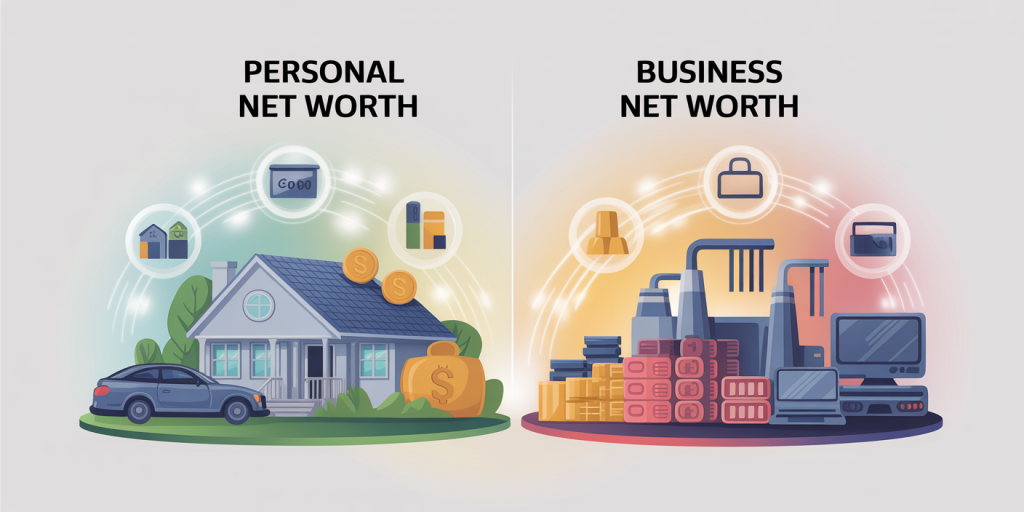

Net Worth and Business Valuation: Differences and Similarities

While net worth is commonly used for personal finance, it is equally important in business contexts, though with some nuances. In business, a similar measure known as “owner’s equity” represents the residual interest in assets after liabilities.

For example, a small business may have assets including property, equipment, and inventory, balanced against loans and accounts payable. The owner’s equity or business net worth helps determine financial health, creditworthiness, and valuation for potential investors or buyers.

Consider a startup company with $500,000 in assets and $300,000 in liabilities. Its net worth is $200,000, which might indicate positive progress, but profitability, cash flow, and growth potential must also be assessed.

Below is a comparison table highlighting key differences between personal net worth and business net worth:

| Aspect | Personal Net Worth | Business Net Worth (Owner’s Equity) |

|---|---|---|

| Assets | Homes, savings, investments | Equipment, inventory, cash |

| Liabilities | Loans, mortgages, credit cards | Loans, accounts payable, accrued expenses |

| Purpose | Financial health and goals | Business valuation and operations |

| Volatility | Generally stable | Often more volatile due to operational risks |

| Measurement Frequency | Typically annual or quarterly | Often monthly or quarterly |

Understanding these distinctions helps entrepreneurs manage personal and business finances separately yet strategically.

Strategies to Improve Net Worth

Improving net worth requires a balanced approach focusing on increasing assets and reducing liabilities. Here are key strategies with examples:

1. Increase Savings and Investments: Regularly contributing to savings accounts, retirement plans, and diversified investment portfolios builds asset value over time. For instance, investing $5,000 annually in a balanced portfolio averaging 7% annual return can grow significantly over 20 years.

2. Pay Down High-Interest Debt: Prioritize paying off credit card debt and personal loans, as these liabilities can erode net worth via interest payments.

3. Build Home Equity: Owning property and making mortgage payments can increase home equity, a substantial portion of many Americans’ net worth. Refinancing at lower rates can also reduce liabilities.

4. Monitor and Adjust Spending Habits: Budgeting, reducing unnecessary expenses, and avoiding lifestyle inflation free up funds to reduce debt and increase savings.

5. Regular Assessment: Using tools like personal finance software or working with a financial advisor ensures consistent tracking and timely decision-making.

For example, Michelle, a 40-year-old professional with $100,000 in credit card debt and $150,000 in assets, focused on aggressive debt repayment while investing to increase asset growth. Over five years, her net worth shifted from slightly negative to positive $75,000.

Future Perspectives: The Changing Landscape of Net Worth in a Financially Dynamic World

The importance of understanding net worth will only grow as global economic conditions evolve, influenced by factors such as inflation, technological shifts, and changing labor markets. Inflation rates, which have fluctuated from the lows of the 2010s to spikes in recent years (e.g., U.S. inflation peaking near 9.1% in mid-2022), can erode purchasing power and alter asset valuations, making real net worth calculations essential.

Emerging trends like digital assets—cryptocurrencies and NFTs—bring complexity to net worth calculations, requiring individuals to reassess how these volatile assets fit within their financial landscape.

Furthermore, demographic changes with longer life expectancies mean sustained financial planning is crucial to maintain positive net worth during extended retirement years.

Financial literacy programs emphasizing net worth awareness and management will become increasingly important. Governments and financial institutions may develop advanced tools and platforms for real-time net worth tracking, integrating AI for personalized advice.

In essence, net worth remains a crucial pillar of financial planning, and adapting to future challenges while leveraging technology will empower individuals and businesses to enhance financial resilience and prosperity.

Understanding net worth not only clarifies your present financial situation but empowers you to make informed decisions and craft pathways toward wealth accumulation and security. By regularly evaluating assets, liabilities, and market conditions, and implementing proven strategies, achieving a strong and sustainable net worth becomes an attainable and measurable goal.