In today’s consumer-driven economy, payment methods have evolved dramatically, profoundly influencing spending behavior. Among the most striking observations is the distinct psychological difference between paying with cash and paying with cards. Many consumers report that swiping or tapping a card feels less painful than handing over physical cash, which can lead to increased spending or decreased financial awareness. This phenomenon, often referred to as the “pain of paying,” is crucial to understanding consumer psychology and financial management.

Understanding the Psychological Concept of Pain of Paying

The “pain of paying” refers to the emotional and cognitive discomfort felt when parting with money. This pain acts as a psychological deterrent, encouraging more prudent spending by making the act of paying consciously unpleasant. Cash payments intensify this sensation because they provide immediate, tangible feedback—one can physically see and feel the money leaving their possession, which anchors the awareness of loss.

Card payments, conversely, tend to obscure the immediacy and tangibility of the transaction. When consumers use credit or debit cards, the payment is abstracted, often delayed, or less visible. This intangible experience tends to decouple the spending from the money “pain point,” making it easier to part with funds and potentially leading to overspending.

A 2016 study by behavioral economists Prelec and Loewenstein revealed that when consumers use cash, their brain shows stronger emotional reactions centered around loss and spending avoidance. In contrast, card payments activate areas of the brain linked to rewards and delayed gratification, reducing the emotional sting of spending.

Cash vs. Card: Behavioral Patterns in Spending

To highlight the practical impact of payment methods, consider a real-world example from a 2019 experiment conducted by the Bank of Canada. Researchers observed that shoppers spent 22% more when using credit cards instead of cash, underscoring the strong relationship between payment mode and spending behavior.

Cash spending forces immediate budget reassessments. For instance, a person handing over a $50 bill at a store becomes instantly aware of the money leaving their hands, making them more likely to reevaluate additional purchases. Meanwhile, when using a card, the same person is less conscious of immediate payment, which can encourage impulsive buys or higher spending.

Further supporting this distinction, a 2018 survey by the National Endowment for Financial Education (NEFE) found that 56% of Americans feel less control over their finances when paying by card compared to cash. The survey also identified that consumers using cards regularly worry more about overspending and accumulating debt.

| Payment Method | Spending Increase (%) | Psychological Impact | User Perception of Control |

|---|---|---|---|

| Cash | Baseline | High pain of paying, tangible loss | Higher sense of spending control |

| Credit/Debit Card | +22 | Lower pain of paying, abstract loss | Lower sense of control |

This comparison table summarizes the primary contrasts between cash and card payments, illustrating why card use may decrease the pain of paying.

Cognitive Mechanisms Behind Card Payment Ease

Why does using cards reduce the pain of paying? Several cognitive mechanisms explain this phenomenon:

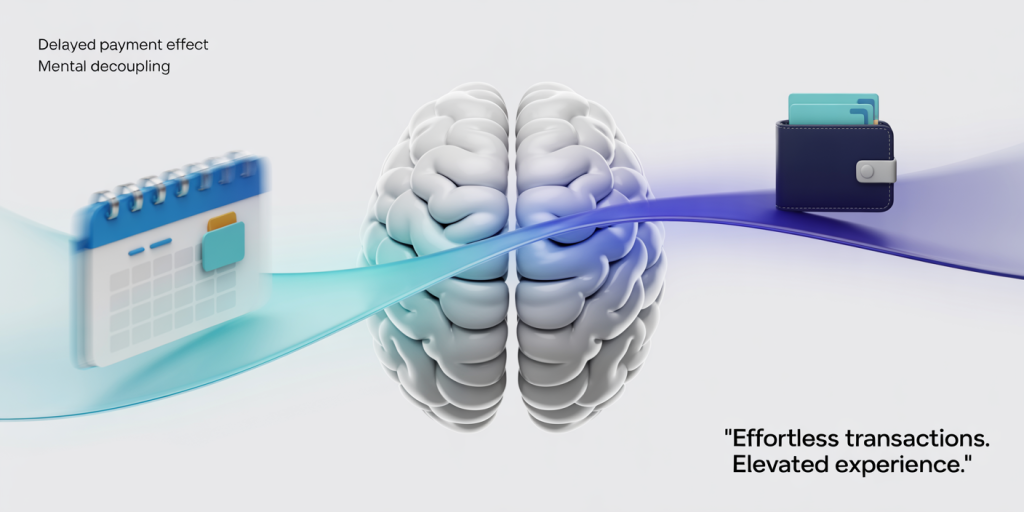

1. Delayed Payment Effect Credit cards, in particular, introduce a temporal gap between purchase and payment, dissociating the act of spending from immediate financial sacrifice. This delay blurs the mental recognition that money is leaving the individual’s funds, reducing spending hesitation.

2. Decoupling and Mental Accounting Card transactions often appear as abstract numbers on a screen or monthly statements rather than physical cash leaving the wallet. This mental decoupling alters mental accounting—where budgets and spending categories are managed psychologically—making it easier to spend beyond immediate means.

3. Reward Systems Activation Neurological studies show that card use activates reward centers more intensely than cash, as buying with a card can feel more like “gaining” than “losing,” especially with rewards such as cashback or points. For example, credit card reward programs encourage consumers to view purchases as opportunities for benefits rather than financial outflows.

A practical case is Amazon’s success with 1-Click checkout, where the reduction in friction during payment led to increased purchase frequency and average basket size by up to 10%. The ease of card spending facilitated part of this increase.

The Impact of Payment Type on Financial Health

While card payments provide convenience and often security, the diminished pain of paying has tangible risks for personal financial health. Overspending and debt accumulation are common byproducts.

The Federal Reserve’s 2021 Consumer Credit Report highlighted that total consumer credit reached $4.4 trillion, with credit card debt representing a significant portion. Many analysts attribute this growth partially to the ease of card spending and the reduced pain of paying.

Additionally, a study in the Journal of Consumer Research (2019) found that consumers paying with cards reported higher levels of regret post-purchase than cash payers, indicating awareness issues and emotional consequences linked to reduced payment pain.

Case in point: Millennials and Gen Z consumers, who heavily favor digital and card payments, experience higher overall indebtedness rates than older generations who traditionally used cash or checks more frequently.

Financial advisors often recommend cash budgeting systems or using prepaid cards to increase the pain of paying and improve spending discipline. Such techniques ring-fence budgets by restoring the physical or mental visibility of spending limits.

Technological Innovations and the Future of Payment Pain

As payment technology evolves, the psychological dynamics around spending are also transforming. Contactless payments, mobile wallets, and cryptocurrencies introduce new layers of abstraction, potentially amplifying the ease of spending yet further.

For example, contactless payment use rose by 150% worldwide between 2019 and 2023, according to the World Payments Report. The frictionless nature of tapping a phone or card enhances convenience but can simultaneously reduce the pain of paying even more than traditional swipe or chip transactions.

Moreover, subscription-based models empowered by digital payment ease increase “invisible” recurring expenses, further distancing consumers from active payment decisions. Netflix, Spotify, and other subscription services exemplify this shift, where payments are automatic and often overlooked, causing consumers to lose track of overall spending.

However, fintech innovations are attempting to rebalance this equation. Spending analytics, real-time notifications, and AI-driven budgeting tools aim to increase financial awareness by reconnecting consumers with their spending decisions. Apps like Mint, YNAB (You Need A Budget), and others provide more immediate feedback and cater to enhancing the pain of paying through behavioral nudges.

Looking Ahead: Balancing Convenience with Financial Mindfulness

The future of payment methods will likely continue emphasizing speed, convenience, and security, further reducing the traditional pain of paying. However, the growing consumer debt levels and financial stress underscore the urgent need for solutions that restore mindful spending habits.

Emerging trends suggest a balanced approach: integrating “smart friction” in payment experiences to prevent unconscious overspending without diminishing convenience. This could include adaptive payment flows requiring deliberate confirmation for high-value transactions or embedding automated spend alerts tied to personal budgeting goals.

Beyond technology, financial literacy programs must adapt to educate populations on how payment modes affect behavior and financial outcomes. Empowering consumers with this psychological insight can foster healthier financial habits.

In summary, while card spending feels easier because it reduces the pain of paying through cognitive and emotional mechanisms, awareness of this phenomenon is vital to preventing negative financial impacts. The intersection of psychology, technology, and financial education will shape the next generation of payment solutions and spending behaviors.