In the world of personal finance, understanding credit scores is essential for making informed financial decisions. Credit scores influence everything from loan approvals and interest rates to renting apartments and even job applications. However, the mechanics behind how credit scores work remain a mystery to many. This article delves into the intricate world of credit scores, explaining their composition, significance, and impact on everyday financial life.

The Foundation of Credit Scores: What They Represent

A credit score is a numerical representation of an individual’s creditworthiness—a measure that lenders use to assess the risk associated with lending money. Credit scores typically range from 300 to 850, where higher scores indicate better credit behavior. These numbers are derived from detailed information contained in a person’s credit report, which compiles data from various sources, including banks, credit card companies, and public records.

To put this into perspective, imagine two individuals applying for a mortgage. One has a credit score of 780, while the other has a score of 620. The first applicant is more likely to receive approval and preferable loan terms due to a high probability of timely repayments. Conversely, the second applicant may face higher interest rates or even rejection because lenders perceive a higher risk.

According to Experian, one of the major credit bureaus, the average FICO credit score in the United States was around 716 in 2023. This figure gives a benchmark for understanding where most consumers fall and highlights how crucial it is to maintain a good credit score to access affordable credit.

Key Factors That Shape Your Credit Score

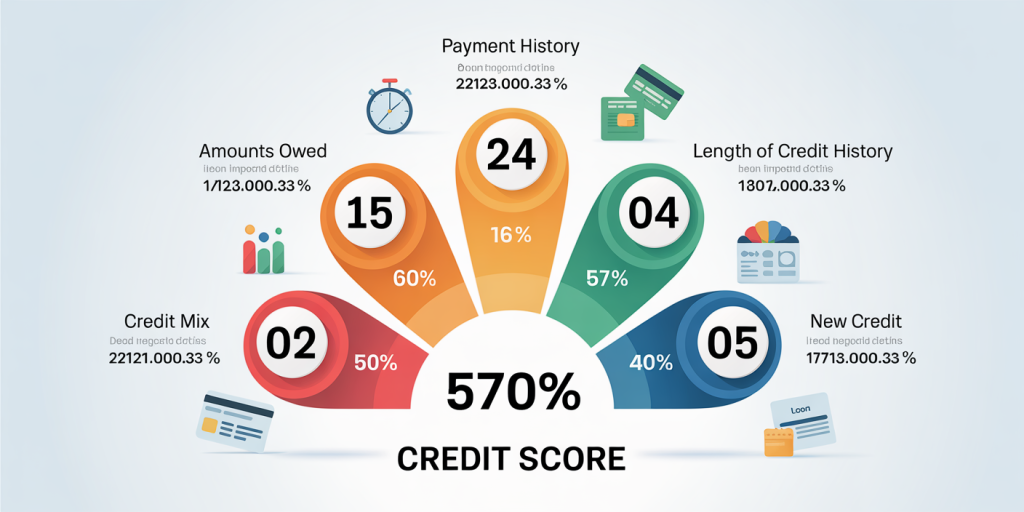

Credit scores are calculated using various factors that reflect an individual’s credit behavior. The most commonly used scoring model, FICO, breaks these components into five primary categories:

1. Payment History (35%) 2. Amounts Owed (30%) 3. Length of Credit History (15%) 4. Credit Mix (10%) 5. New Credit (10%)

Payment History: The Most Critical Component

Payment history accounts for over a third of your credit score, making it the most influential factor. This category assesses whether you pay your bills on time, including credit cards, loans, mortgages, and utilities. Even a single late payment can cause a significant drop in a credit score, especially if overdue by more than 30 days.

Consider the case of a borrower who missed a credit card payment by 45 days. This late payment appeared on their credit report and reduced their score by approximately 50 points, leading to a denied car loan application several months later. This example underscores why timely payments are paramount.

Amounts Owed and Utilization Rates

Amounts owed refers to how much debt you currently carry, particularly in relation to your credit limits—known as the credit utilization ratio. Keeping credit card balances low relative to credit limits helps improve scores. Experts recommend maintaining utilization below 30%.

For instance, a consumer with a credit card limit of $10,000 and a balance of $2,000 has a utilization rate of 20%, which is seen as healthy. If the same individual increased their balance to $8,000, pushing utilization to 80%, this could lower their credit score significantly.

| Factor | Description | Impact on Credit Score (%) |

|---|---|---|

| Payment History | Timeliness of bill payments | 35% |

| Amounts Owed | Credit utilization percentage | 30% |

| Length of Credit History | Duration of credit accounts | 15% |

| Credit Mix | Variety of credit types | 10% |

| New Credit | Recent credit inquiries and openings | 10% |

Understanding Different Types of Credit Scores

There are various types of credit scores, with the FICO score being the most widely used by lenders. Another popular model is the VantageScore, developed collaboratively by the three main credit bureaus: Experian, TransUnion, and Equifax. While they operate similarly, there are subtle differences in how they weight factors or treat specific data points.

For example, VantageScore models tend to be more forgiving of consumers with limited credit history and can generate scores earlier than FICO, which may require at least six months of credit data. In contrast, FICO remains the go-to model for mortgage lenders and most major credit assessments.

Additionally, industry-specific scores exist that cater to certain lending types, like auto loans or credit cards. These specialized scores tweak the weighting of factors to better gauge risk for specific financial products.

Practical Impacts of Credit Scores on Financial Life

The influence of credit scores extends beyond the ability to borrow money. Your credit score affects interest rates, insurance premiums, and even employment prospects. Statistics from the Consumer Financial Protection Bureau (CFPB) indicate that individuals with higher credit scores typically pay 20% to 30% less in interest on loans than those with lower scores.

Loans and Interest Rates

Lenders use credit scores to determine eligibility and pricing on loans. For instance, a prime credit score (above 740) will usually unlock the best mortgage rates, whereas a subprime score (below 620) may only allow access to loans with higher interest rates—or none at all.

Consider two applicants for a $250,000 mortgage:

| Credit Score Range | Estimated Interest Rate | Monthly Payment (30-year fixed) | Total Interest Paid |

|---|---|---|---|

| 760 – 850 | 3.0% | $1,054 | $130,480 |

| 620 – 659 | 5.5% | $1,420 | $261,440 |

The difference in interest totals more than $130,000 over the life of the loan, illustrating how credit scores affect affordability.

Renting and Employment

Landlords frequently use credit scores to screen potential tenants, as a reliable credit history signals financial responsibility. Similarly, some employers check credit reports during the hiring process, particularly for roles handling money or sensitive data, to evaluate a candidate’s reliability.

Common Myths and Misunderstandings About Credit Scores

Many misconceptions about credit scores persist, often causing individuals to make poor financial choices. For instance, some believe that checking their own credit score harms it. This is false; personal inquiries are classified as “soft” pulls and do not affect scores.

Another myth suggests that closing old credit accounts can boost scores. In reality, closing accounts reduces your overall credit limit and shortens credit history, potentially lowering your score. It’s often better to keep old accounts open, especially if they have good payment records.

Likewise, paying off a collection account does not automatically remove it from your credit report. The collection will remain for up to seven years but may update to “paid,” which lenders view more favorably.

Building and Maintaining a Strong Credit Score

Building or repairing a credit score requires consistent and responsible credit behavior. The first step is to ensure timely payments on all debts—this is the backbone of credit health. Next, keep credit utilization low by avoiding maxing out credit cards.

Another useful strategy is diversifying credit type; having a mix of revolving accounts (credit cards) and installment loans (mortgages, car loans) can help improve scores. However, opening many new accounts in quick succession can backfire by triggering multiple hard inquiries, which may signal desperation to lenders.

It’s also important to review credit reports regularly to spot errors or fraudulent activity. The federal government mandates that consumers receive a free credit report annually from each of the three major bureaus via AnnualCreditReport.com. Disputing inaccuracies with credit bureaus can lead to corrections that improve scores.

The Future of Credit Scoring: Trends and Innovations

Credit scoring is evolving rapidly with advancements in financial technology and data analysis. Traditional scoring models rely heavily on historical credit data, but newer approaches aim to incorporate alternative data sources for a more comprehensive assessment.

For example, some fintech companies consider utility payments, rental history, and even cash flow data from bank accounts to evaluate creditworthiness, especially for those with thin or no credit files. This approach has the potential to bring millions of underserved individuals into mainstream credit markets.

Machine learning algorithms are also being deployed to develop more nuanced risk models, reducing bias and increasing predictive accuracy. According to a 2023 report by McKinsey, incorporating alternative data can increase loan approval rates by 20% without raising default risk.

Privacy concerns and regulatory scrutiny will shape the future of credit scoring, demanding transparency and fairness in how data is collected and used. Innovations like blockchain could offer consumers greater control over their financial data, allowing for secure and verifiable sharing with lenders.

As credit systems shift towards more inclusive and technology-driven models, consumers stand to benefit from fairer evaluations and expanded access to credit, provided they remain informed about their credit standing and financial behavior.

—

Understanding how credit scores work empowers consumers to make smarter financial choices and avoid costly pitfalls. Maintaining a strong credit profile demands awareness, discipline, and proactive management but opens doors to better financial opportunities and security. As the credit landscape transforms, staying updated with credit trends and utilizing new tools will offer even greater control over one’s financial future.