In today’s financial landscape, managing multiple debts can become overwhelming and stressful. According to the Federal Reserve, as of 2023, American household debt reached over $16 trillion, with credit card debt alone exceeding $930 billion. High-interest rates and compound interest can increase the total amount owed significantly over time, making debt repayment a prolonged struggle for many individuals. Debt consolidation offers a strategic solution to simplify debt management and potentially save money. However, doing it smartly is crucial to avoid pitfalls such as accumulating more debt or encountering unfavorable loan terms. This article provides actionable guidance on how to consolidate debt effectively and responsibly, drawing from real-life examples, expert insights, and comparative analysis.

Understanding Debt Consolidation: What It Entails and Why It Matters

Debt consolidation is the process of combining multiple outstanding debts into a single loan or payment plan, typically with a lower interest rate or more manageable monthly payments. The primary goal is to streamline payments, reduce interest costs, and improve financial clarity. For example, instead of juggling five different credit card bills, one might consolidate those balances under a personal loan or balance transfer credit card with one monthly payment.

It’s important to differentiate between debt consolidation and debt settlement. While consolidation restructures existing debts, settlement involves negotiating a reduced payoff, often negatively impacting credit scores. Smart debt consolidation maintains the original balance and improves repayment terms, allowing borrowers to pay off the full debt sum more efficiently. This approach helps avoid the penalty risks associated with settlements and bankruptcy, which according to a 2022 report from the Consumer Financial Protection Bureau (CFPB), adversely impacts creditworthiness in 70% of cases for years.

Choosing the Right Debt Consolidation Method

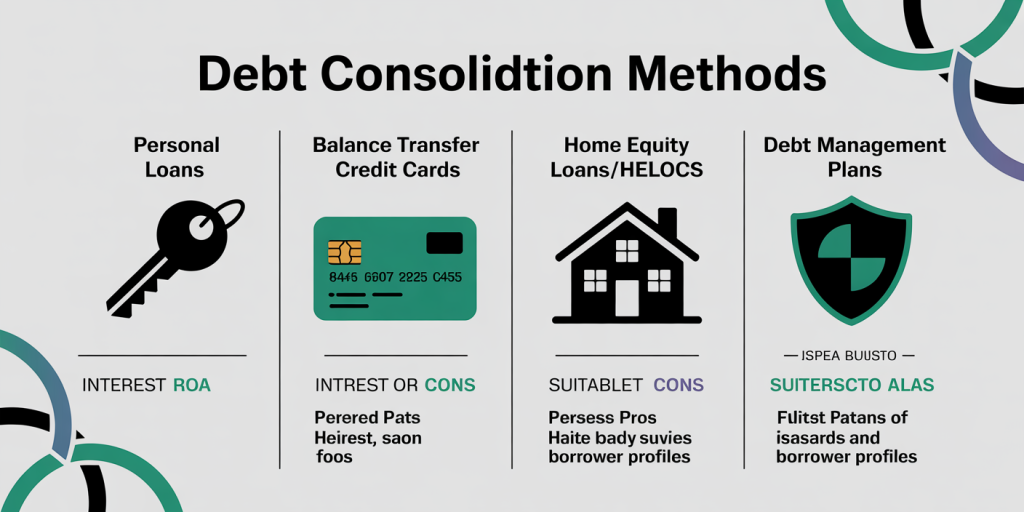

Multiple approaches to debt consolidation exist, each with distinct advantages and risks. The key is assessing your financial situation, credit score, and debt profile before selecting a method.

Personal Loans

Personal loans for debt consolidation typically come with fixed interest rates and set repayment terms. Borrowers with strong credit scores (generally 700+) can access loans with interest rates ranging from 6% to 15%, significantly lower than typical credit card APRs hovering around 20%. An example is Sarah, a 32-year-old professional who consolidated $18,000 credit card debt with a 10% APR personal loan. Over three years, she saved nearly $3,000 in interest while lowering monthly payments from $650 to $520.

Balance Transfer Credit Cards

These credit cards offer 0% APR introductory periods, usually lasting 12 to 18 months, allowing borrowers to pay off debt interest-free during that window. However, the catch lies in the balance transfer fees—typically 3-5% of the transferred amount—and the high APR after the promotional period ends. For example, John consolidated $10,000 credit card debt using a balance transfer card with a 15-month 0% APR offer and a 3% fee, effectively adding $300 upfront but saving over $2,000 in interest. He then paid off the balance within the promotional period to avoid high post-introductory interest rates.

Home Equity Loans and Lines of Credit (HELOCs)

Using home equity can reduce interest rates substantially—sometimes as low as 4-7%. However, this method converts unsecured debt into secured debt, putting the home at risk if repayments are missed. For families with a stable income and sufficient equity, this can be an effective solution. A case study by Zillow in 2023 revealed that 40% of borrowers who used HELOCs for debt consolidation reported confidence in paying off debt faster with significant interest savings.

Debt Management Plans (DMPs)

Offered by credit counseling agencies, these plans consolidate debts into one monthly payment managed by the agency. They may negotiate lower interest rates or fees with creditors but require strict adherence to their repayment terms. According to the National Foundation for Credit Counseling, about 75% of clients completing DMPs become debt-free within 4-5 years.

| Consolidation Method | Typical Interest Rate | Pros | Cons | Suitable For |

|---|---|---|---|---|

| Personal Loans | 6% – 15% | Fixed rates, predictable payments | Credit score dependent | Good credit, multiple debts |

| Balance Transfer Cards | 0% intro for 12-18 months | Interest-free period, flexible | Balance transfer fees, high post-intro rate | Short-term payoff, creditworthy borrowers |

| Home Equity Loans/HELOCs | 4% – 7% | Low interest, tax benefits | Puts home at risk, fees | Homeowners with equity |

| Debt Management Plans | Varies | Professional help, negotiated rates | Requires discipline, long commitment | Those struggling with multiple debts |

Evaluating Your Financial Health Before Consolidating

Smart consolidation begins with a clear understanding of your existing financial situation. Track all debts, interest rates, minimum payments, and repayment periods. Using tools such as Mint or YNAB (You Need A Budget) can help create a comprehensive overview. This data supports selecting the most cost-effective consolidation method.

Credit score plays a pivotal role in consolidation success. According to FICO, borrowers with scores above 700 tend to qualify for better rates and terms, reducing total interest costs by up to 30%. Those with poor credit may face higher costs or might need alternative strategies like credit counseling or secured loans.

Calculate the total interest and fees for each potential consolidation option and compare against the current debt costs. One tool recommended by experts at NerdWallet is the Debt Repayment Calculator, which simulates different strategies over time.

Steps to Consolidate Debt Effectively

To consolidate debt smartly, follow a disciplined multi-step approach:

1. List and Prioritize Debts: Rank debts by interest rate and balance. High-interest debts like credit cards should typically be prioritized for consolidation.

2. Assess Available Options: Research loans, credit cards, and counseling options to find suitable offers. Prequalification tools can help estimate rates without impacting credit scores.

3. Calculate True Costs: Factor in fees such as loan origination charges, balance transfer fees, or early payment penalties. Consider both monthly payment affordability and total repayment cost.

4. Apply and Verify Terms: Carefully review loan contracts or agreements, focusing on interest rate, repayment period, and flexibility. Clarify penalty policies in case of missed payments.

5. Avoid New Debt: During and after consolidation, avoid increasing debt balances to prevent undoing progress. Some people fall into a cycle where consolidation provides relief but encourages further borrowing.

For example, Alexa, a 45-year-old teacher, consolidated $25,000 of credit card debt into a personal loan after comparing offers from five lenders. She noted that a 7-year loan term lowered monthly payments to $415, compared to her previous $650, giving room in the budget for emergency savings.

Potential Pitfalls and How to Avoid Them

Despite its advantages, debt consolidation has inherent risks and traps. One major challenge is extending repayment terms too long, which could increase total interest paid despite lower monthly payments. According to a 2023 study by the Urban Institute, borrowers extending loan terms beyond five years paid 20-25% more interest overall, despite improved cash flow.

Another pitfall is complacency after consolidation, leading to new spending on credit cards. Financial experts advise closing paid-off credit card accounts or freezing their usage to maintain discipline.

Watch out for scams as well. The Federal Trade Commission (FTC) warns about debt consolidation companies that charge upfront fees without delivering results. Legitimate debt consolidation programs usually have clear fee structures and accreditation.

Finally, tax implications should be considered. For example, cancelation of debt in certain cases may be treated as taxable income by the IRS, as highlighted in IRS Publication 4681. However, consolidations via loans generally don’t trigger tax events.

Looking Ahead: The Future of Debt Consolidation

With the rise of fintech innovations, the future of debt consolidation is shifting toward more accessible, transparent, and personalized solutions. AI-powered financial advisors and digital lending platforms provide instant prequalification and customized loan offers based on data analytics.

Moreover, regulatory changes are focusing on consumer protections to reduce predatory lending practices. For instance, the Consumer Financial Protection Bureau is proposing rules to enhance transparency around loan terms and debt consolidation offers, promoting informed decision-making.

Sustainability and financial wellness integration are becoming prominent trends. Employers increasingly offer debt consolidation assistance as part of employee benefits, and apps once focused solely on budgeting now incorporate debt payoff coaching integrated with consolidation options.

Digitally enhanced debt consolidation may also incorporate behavioral nudges and educational tools to prevent relapse into poor financial habits, a significant issue in the current environment. Research from the FINRA Investor Education Foundation reveals that 60% of consumers experience difficulty maintaining long-term debt reduction without guidance.

In summary, consolidating debt smartly involves a combination of thorough financial evaluation, selection of an appropriate method, cautious cost comparison, and a commitment to financial discipline. As tools and regulations evolve, consumers will have more effective means to manage debt constructively, paving the way to financial stability and improved credit health. By leveraging technology and expert guidance, individuals can tailor solutions to their unique situations and avoid common pitfalls that undermine consolidation efforts.