The Pain of Paying: Why Card Spending Feels Easier

In today’s consumer-driven economy, payment methods have evolved dramatically, profoundly influencing spending behavior. Among the most striking observations is the distinct psychological difference between paying with cash and paying with cards. Many consumers report that swiping or tapping a card feels less painful than handing over physical cash, which can lead to increased spending or […]

How Emotions Affect Spending

Emotions play a critical role in shaping consumer behavior, influencing how individuals make financial decisions, including their spending patterns. The connection between feelings and expenditures has been studied extensively, revealing that emotions can drive impulsive purchases, delay necessary spending, or even trigger financial regret. This article delves into the complex relationship between emotions and spending, […]

How Emotions Affect Spending

Emotions play a critical role in shaping consumer behavior, influencing how individuals make financial decisions, including their spending patterns. The connection between feelings and expenditures has been studied extensively, revealing that emotions can drive impulsive purchases, delay necessary spending, or even trigger financial regret. This article delves into the complex relationship between emotions and spending, […]

What Is Lifestyle Creep?

As individuals progress in their careers and increase their incomes, a phenomenon known as “lifestyle creep” often begins to subtly shape their spending habits and financial decisions. Lifestyle creep, sometimes called lifestyle inflation, refers to the gradual increase in one’s spending as income rises. This incremental shift in living standards may seem harmless or even […]

The Role of Central Banks

Central banks are pivotal institutions within the global financial architecture, influencing economic stability, inflation control, and monetary policy. These entities dictate much of the financial environment that affects individuals, businesses, and governments. Understanding the role of central banks provides insights into how economies operate, how financial systems maintain trust, and how economic crises are mitigated. […]

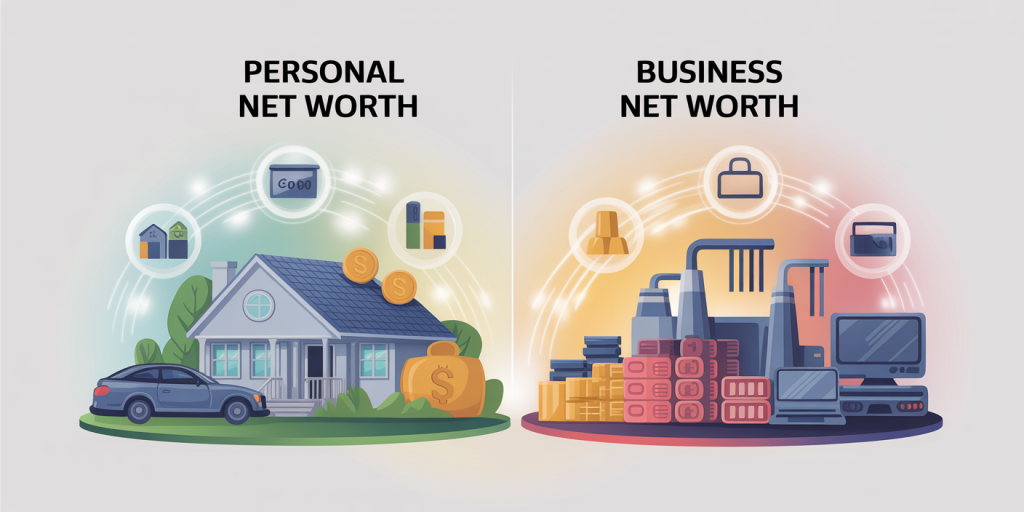

Understanding Net Worth: A Comprehensive Guide to Financial Health

Net worth is an essential financial metric that serves as a vital indicator of an individual’s or organization’s fiscal condition. Whether you are planning for retirement, managing personal finances, or running a business, understanding your net worth can help you make informed decisions, gauge progress toward financial goals, and prepare for uncertainties. This article delves […]

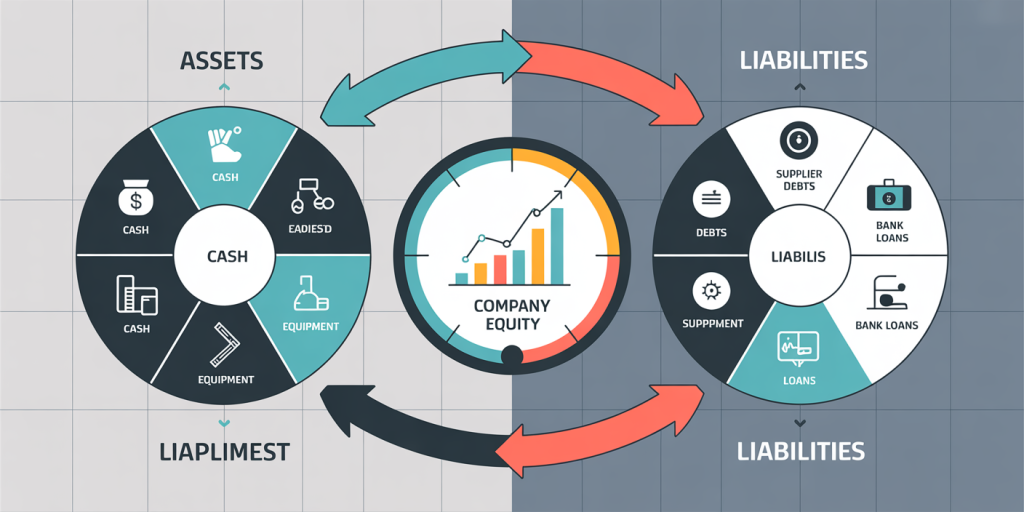

Difference Between Assets and Liabilities

In the world of finance and accounting, understanding the distinction between assets and liabilities is fundamental. These two concepts form the backbone of financial statements and play a critical role in evaluating an organization’s financial health. Whether you are a business owner, investor, or student of finance, mastering the difference between assets and liabilities can […]

How the Banking System Works

Understanding the banking system is crucial for anyone interested in economics, finance, or simply managing personal finances effectively. Banks play a vital role in the economy by facilitating financial transactions, providing loans, and acting as custodians of money. This article explores how the banking system operates, its core functions, the key players involved, and current […]

Inflation Explained Simply

Inflation is a term frequently encountered in discussions about economics, personal finance, and government policy. Yet, despite its widespread use, many people still find it confusing or intimidating. Understanding inflation is essential not only for making informed financial decisions but also for grasping how an economy functions. This article breaks down inflation into simple concepts, […]

How to Stop Comparing Finances with Others

In today’s interconnected world, it is increasingly common for people to measure their financial status against that of their peers, friends, or social media acquaintances. This tendency to compare finances can lead to stress, dissatisfaction, and poor financial decisions. Recent studies have shown that nearly 70% of adults feel financial pressure when comparing themselves to […]